A terrible January can be a source of opportunities

A bad start doesn't have to scare you!

Hello guys,

I hope you are all having good time and that you will enjoy my new outlook on financial markets!

If you are reading this but you haven’t subscribed yet, do it now!

If you want to have full access to two model portfolios (Balanced Portfolio and Pure Stocks Portfolio), please consider to become a paid subscriber of this newsletter.

Let’s talk about markets!

It has been a turbulent January, and many equity indices closed deeply negative, even after a the strong rebound in the last two days.

Who suffered most? Nasdaq, especially growth stocks.

In 2022 the Nasdaq Composite had the worst January since 2008. Just look at the chart below:

As usual, equity performances are linked to the moves of the central banks, so it is fundamental to discuss about that.

Powell: are you a hawk now?

The biggest event of the month has been the press conference of Jerome Powell (on 26th January).

What did he say?

Honestly anything special, except that the FED is ready to use every option to face a more persistent inflation and a strong job market. he added that they will decide meeting by meeting starting from March (no meeting in February). So there is no formal commitment to any decision (like a 50 bps increase in March).

In any case markets have been surprised by his tone, that was resolute, determined, and hawkish.

The reaction has been very strong in the short part of the US yield curve.

As you can see above, the yield of the short term maturities increased sharply, while the long maturities have been not really impacted.

This kind of reaction means that markets are expecting a more aggressive Fed in the stort term. Currently futures are signaling 5 rate hikes in one year. A couple of weeks ago only 4 hikes were discounted:

Even the principal investment banks are changing their estimates, and most of them foresee five or more hikes (BofA has called 7 rate hikes!):

So now markets are positioned for a more hawkish Fed and 5 rates hikes, but will this happen?

Not in my opinion!

Is the U.S. economy slowing down?

In the last free newsletter (that you can find here), I said that inflation growth is close to the peak, but this is not the only reason why I believe the Fed will be more accomodative than expected.

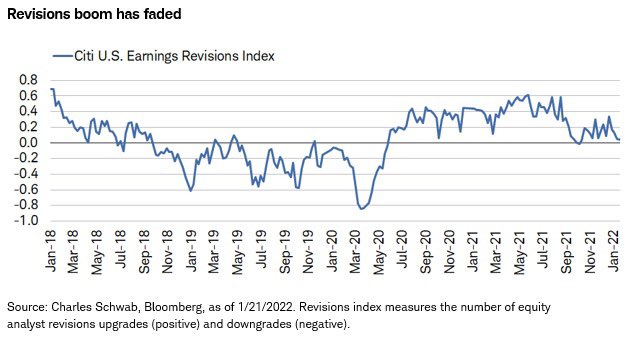

Firstly, the current earning reports are not surprising investors too much.

So far, earnings revisions are at the lowest level since the begin of the pandemic as confirmed from Bank of America and Citi:

Moreover, after the recent macro data, strategists are starting to lower economic projection on U.S. Growth. The last one to do that has been Goldman Sachs:

To sum up, the expectation of a decreasing inflation, not extraordinary earnings and a lower-than-expected growth for the U.S. economy are all factors that are making me believe that Fed officials will be very careful before to make any aggressive move on rates.

I think that the Fed will be more dovish than expected.

Where to invest now?

The subsequent question is: where to invest in this market environment?

In the last market outlook, I wrote that the sell-off on 10-Year Treasury was close to an end, and so far things are going in the right way. In the last few days the 10-Year yield has been in the range 1.75%-1.80%.

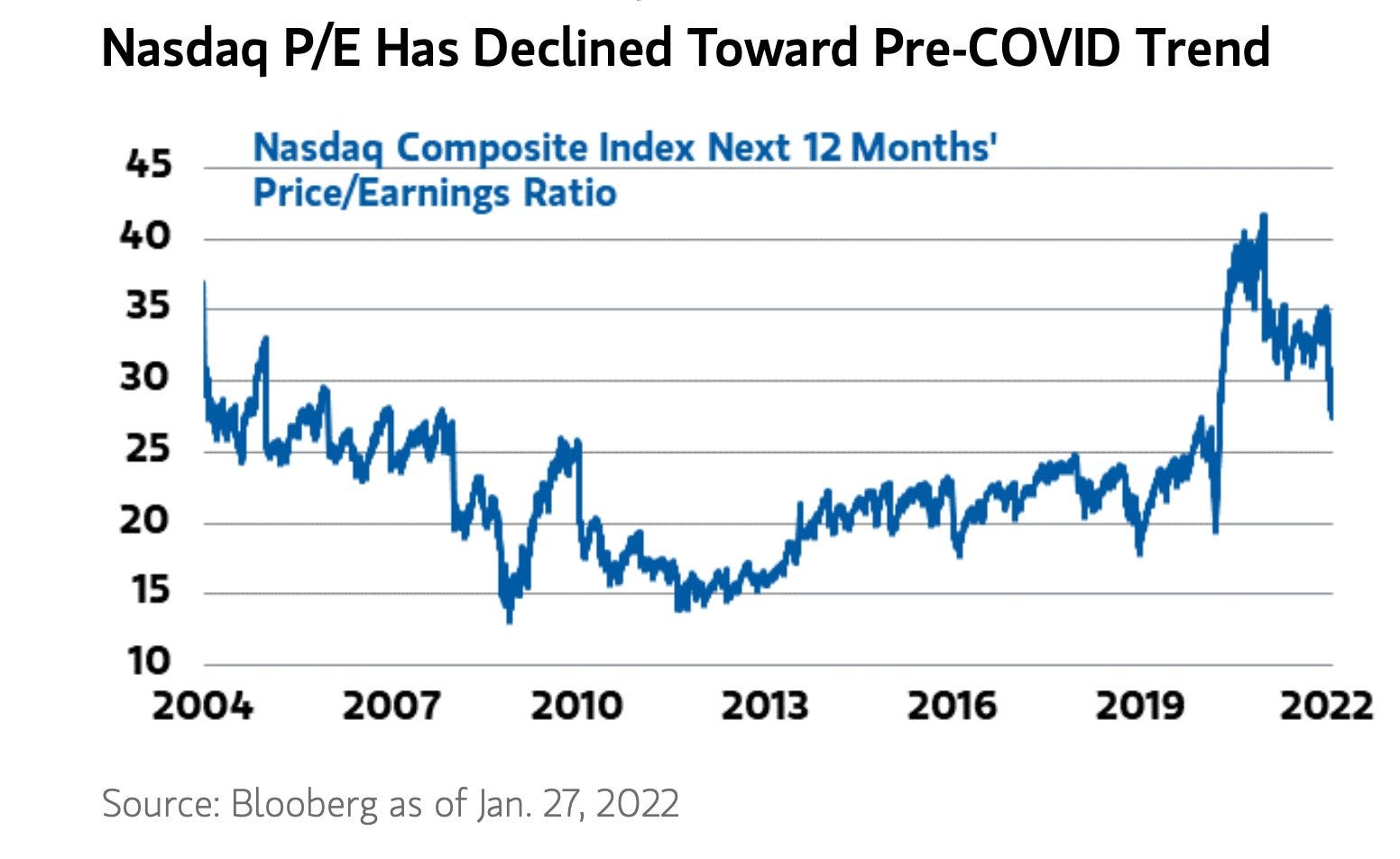

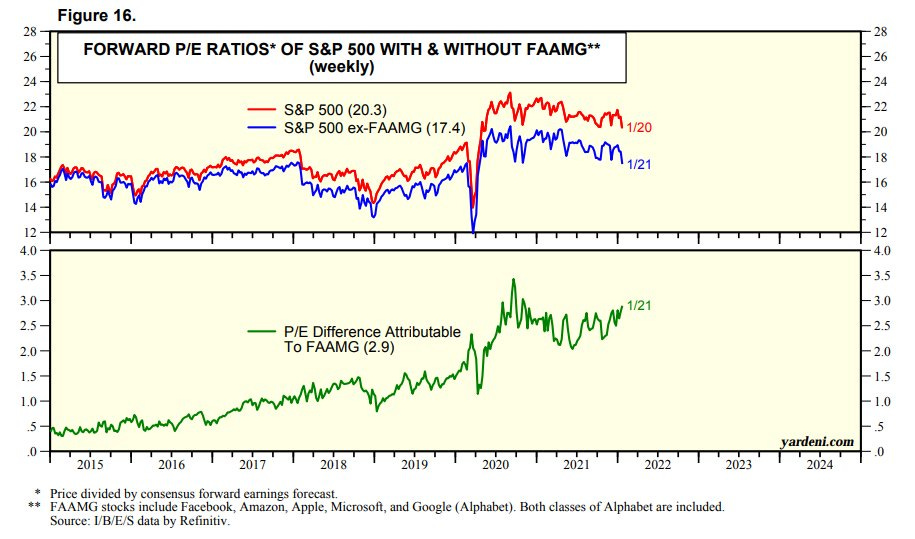

Thanks to a more stable bond market and to more reasonable valuations after the big drawdown (charts below, for Nasdaq and S&P 500), I continue to think that equities is the best area to put your money and obtain positive and good returns.

Markets will probably be turbulent for a while, but the general setup for stocks is still interesting, especially if the Fed will sustain markets with a more cautious approach.

January has been a month of furious rotation on value stocks, that performed much better than growth. I see the overperformance to continue for a while.

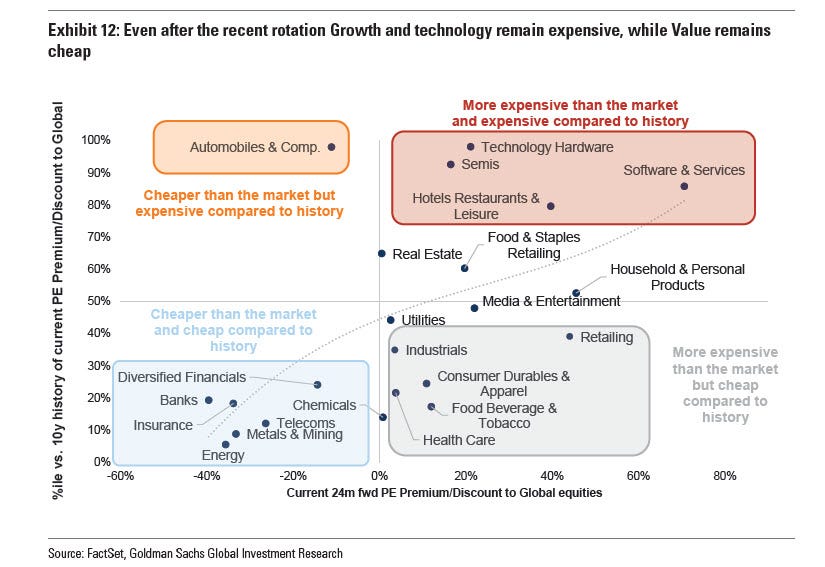

Especially energy stocks continue to have an attractive valuation, both vs market and vs the historical sector valuation, as shown by Goldman Sachs.

In any case, I am becoming everyday more positive on tech and even growth stocks (at the beginning of the year I was very skeptical on them). After the massive sell-off, now there are good opportunities in the growth areas, but it is better to be careful and to size properly every purchase.

I think that the cyclical rotation will continue to boost European equities, especially UK (currently my favorite geographic area).

There are other interesting geographic areas? Yes. I think that emerging markets are in favorable position to gain even if a hiking cycle in U.S. is starting (EM have part of their debt issued in USD, and a stronger USD can be a big problem). Most EM have expanded their USD reserves, and already made several rate increases (as inflation grew). Those factors could make easier for them to navigate in the current markets.

Moreover the MSCI Emerging Markets / S&P 500 Ratio is at its lowest level since 2001. Emerging markets are extremely cheap and it could be a good idea to increase the exposure to them, especially for investors with a long-term horizon.

Finally, I remain neutral on government bonds, but negative on corporate bonds (especially in U.S.), as the spreads, both for IG and HY are starting to increase after months of big compression.

Thank you for your support!

Have a great Week!

Market Radar

If you found the article interesting, please press the like button! It would be really important for the growth of the blog.

Remember: this is not a financial advice! Make your analysis before to make any investment!

Follow my Instagram page if you want to be always updated on last market events.

If you are a long-term investor, Please consider to become a premium subscriber. For a small price, you will have full access to two model portfolios:

Balanced portfolio (here the introduction)

Pure Stock Portfolio (here the introduction)

Moreover you will support my job here and on Instagram!

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.