U.S. vs global equities

Can Europe, Japan, China and Emerging Markets reduce the gap with U.S.?

Hello Guys,

I hope you are fine. As summer holidays are over, I am ready again to analyse the last events and my view on markets.

If you havent’s subscribed to the blog yet, do it now.

Now let’s see what is happening on markets.

August has been another positive month for equities, especially for U.S. Equities, that once again outperformed all the other regions.

If we look at the comparison between S&P 500 and MSCI ACWI (All-Countries index), we can easily notice that the outperformance of the American index is growing month after month.

The only region which is having a comparable path is Europe: the Eurostoxx 600 is up by 17.5% YTD, not far from the +20% return of the S&P 500. Japan and China so far had a completely different path.

In addition to this, as already posted on my Instagram Profile, the reflation trade is having a very long pause, and the growth stocks are overperforming again the value stocks.

In one of the last articles of the blog I wrote that the fear linked to Delta variant could have been bad for cyclical and value stocks, and indeed both performed poorly in the last weeks.

I even warned about a possible (small) correction, that so far it is not happened.

Now we have to ask to ourself what can happen in the next months, and if there is some interesting play to make.

Which indicators can be useful?

One of the figures to check costantly is the 10-Year Treasury Yield for sure.

The main drivers of the Treasury yield are still the same of the last few months: job market, inflation, economic growth and delta variant spread.

Recently, weak data on job market (especially the last Non-farm payroll) have reassured a little bit investors regarding low possibility to see a sooner-than-expected tapering, but this week we already saw good data from Job Openings and Jobless claims. You can understand that the macro environment can change quickly.

It seems that the trend on 10-Year Treasury is reversing, but it is too soon to call.

After a minimum in July, close to 1.15%, the yield is going up again, and approaching a key area at 1.40% (a resistance stands there). The break-out of that threshold could create some tension, on equities too.

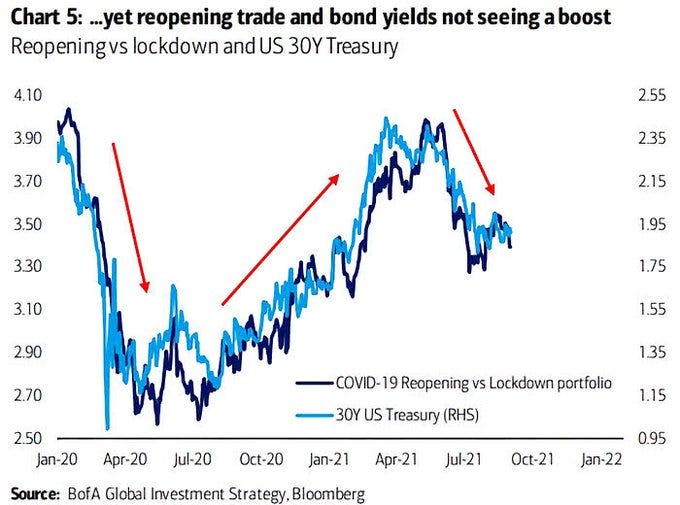

Just as a reminder, look at the correlation between the 30-Year yield and the reflation trade (here called “Reopening portfolio”). You know where the money could go in case of rising rates…

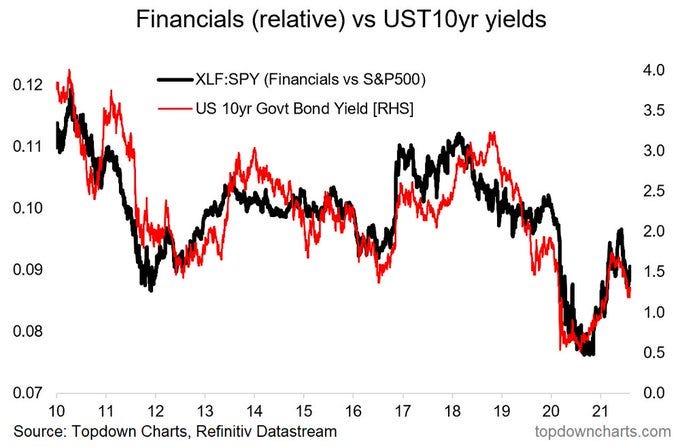

Another one: 10-Year Yield vs Financials/S&P 500.

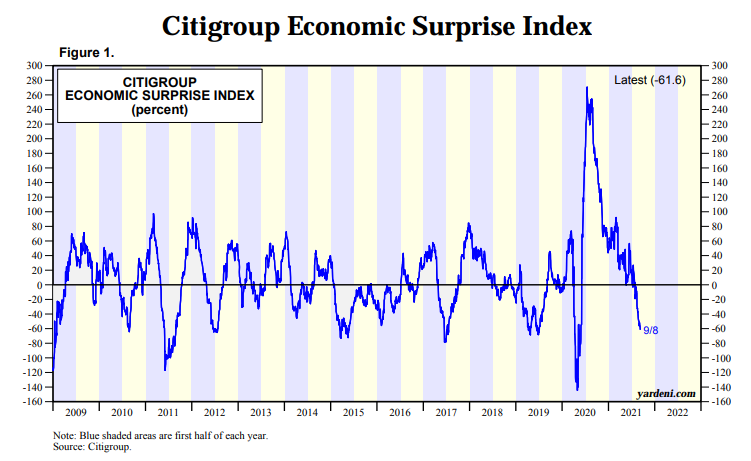

On the other side economic growth is seen decelerating: new data are coming weaker than expected as you can see from the Citi economic surprise index:

Even economists are slowly reducing their forecasts on U.S. Economy, especially for the Q3 2021:

Finally let’s give a look at the Covid situation in developed countries:

New cases are slowing in U.S, Eurozone and Japan, while rising in UK, even if the hospitalizations there remain very low. I see those numbers as positive, even if the cold season is coming, and we could see a temporary worsening.

It is important not to see a strong increase in hospitalization (U.S. are already in a dangerous zone) because it could drive to new restrictions, that could severely impact markets (and normal life!).

Interesting opportunities?

In the current environment I see equity as still the place to be (I don’t really know when bonds will become attractive again), and I would hold any position on U.S. Indices (S&P 500 and Nasdaq), but there are some plays that can be considered in order to diversify your portfolio:

1- Eurozone: As highlighted by several banks (last one Morgan Stanley), European stocks have still a high potential upside. Low Covid cases and high vaccination rate, positive and increasing corporate earnings, low valuations (compared to U.S.) and a still dovish ECB (the recent reduction of PEPP is far from a tapering) are all factors in favour of European stocks. If you want to invest in the entire region you can find an ETF on the Eurostoxx 50 or Eurostoxx 600.

2 - China: the government is still pushing against tech companies, but some of them are taking actions to please the requests of the CCP (Alibaba decided to invest a portion of its income to help China to reach “common prosperity”). Stocks have been hit heavily already, so the risk/reward is attractive.

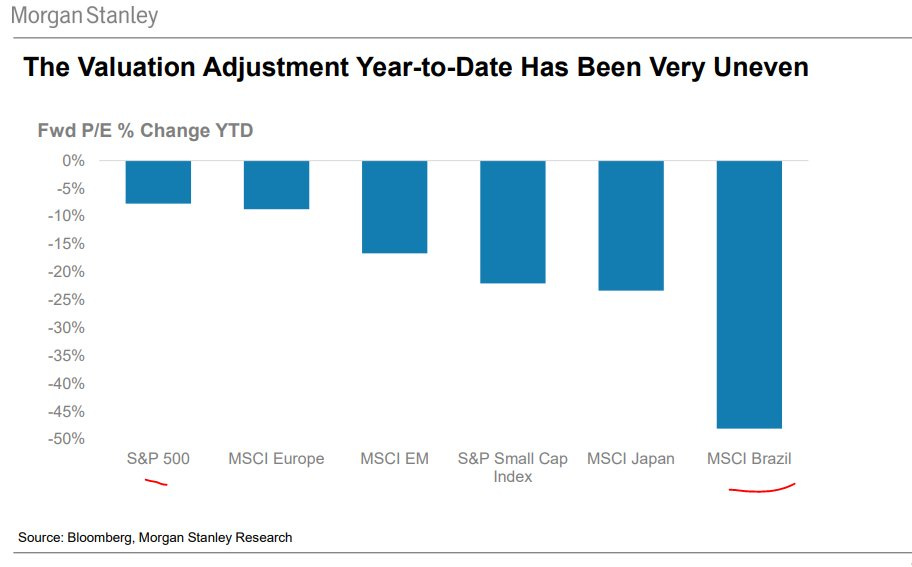

3 - Latin America: in case of a big spike in U.S. Treasury yield the Emerging countries could take a big hit, but as long as rates stay low, emerging markets could be an interesting play, especially Latin America, where the Covid cases are going down a lot, and the high prices of commodities could help many of their companies. Moreover valuations are very compressed. Just look at Brazil P/E change YTD:

4 - Japan: another interesting area is Japan. The current PM, Suga, just stepped down and investors took the news positively. Covid cases are going down, vaccination rate is rising fastly, and recent macro data have been better than expected. Foreign investors are starting to put some money there and maybe it is worth to follow them.

To sum up, U.S. equities dominated so far, but maybe now some regions can narrow the gap with the S&P 500, and overperform for a while. Better to give a look.

Have a great weekend!

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy