The week of the Central Banks: expectations, surprises and reactions

Did JPow stop the Santa Rally?

Hello Guys,

I hope all of you are great and enjoying my articles.

In case you are here but you haven’t subscribed yet, use the button below to do that!

Central bank Party

This week has been crucial for markets. Why? Because some of the most important central banks released their monetary policy expectations for next year.

FED

Let’s start with the Fed!

On Wednesday Powell signaled that inflation is the biggest danger for the U.S. economy, that is now growing good and it is robust.

The Fed will accelerate the tapering (from $15 Bln to $30 Bln) and its officials now expect to raise interest rates three times next year and three times in 2023.

Powell even said that he doesn’t expect a long wait between the end of the asset purchase programme and the first rate hike.

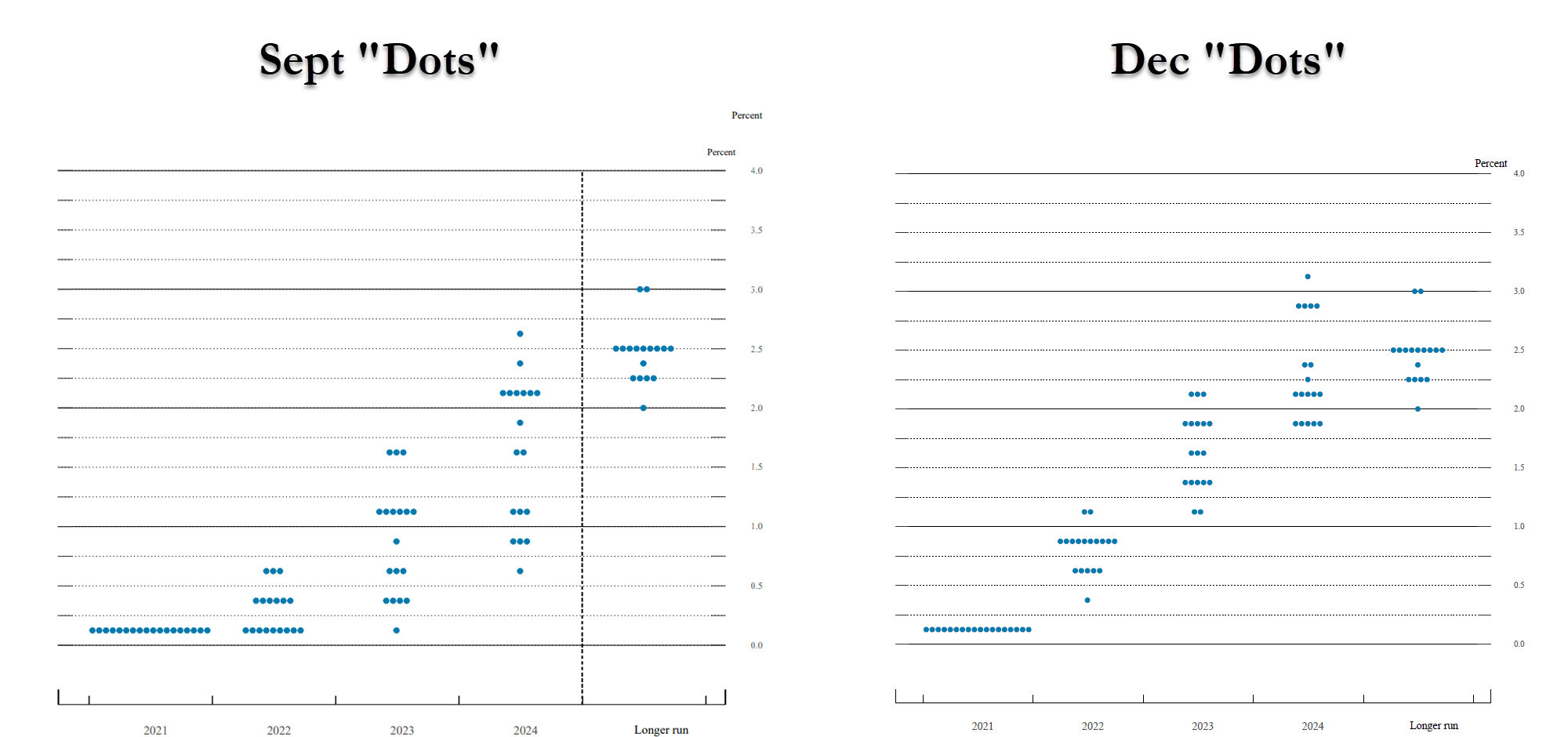

You can see the change of official expectations in the dot plots here below:

It’s quite clear that the Federal Reserve became more hawkish and that inflation is now seen not really transitory.

ECB and BOE

The ECB has been probably the most dovish among the central banks: it left key rates unchanged and it doesn’t foresee to raise them in 2022.

Moreover the ECB decided to increase the Monthly Net purchase pace of the APP (€40 billion in Q2 2022 and to €30 billion in Q3 2022), when the PEPP will end in March 2022. Below you can see clearly how it will work:

Finally, the biggest surprise came from the BOE that decided to raise rates to 0.25%, surprising lot of economists. The bank sees inflation to stay high and persistent, and the officials decided to face that immediately.

The move from BOE could be dangerous, considering that the number of Covid cases is rising sharply. Wel’ll see if they took a good decision.

Turkey Central Bank

Just as an example of what a Central Bank doesn’t have to do when inflation rise: cutting rates.

Probably for religious reasons Erdogan forced the TCB to reduce rates even if inflation was rising (the opposite of what any book suggest).

The result? Inflation is rising even more and the Turkish Lira is a falling knife.

How markets reacted?

You would expect that an hawkish Fed could be very bearish for equities, and bond too. Instead the reaction has been immediately positive.

All the equity indices went initially up, even growth stocks.

The reaction on bonds has been quite tepid too: Treasury yield didn’t make any spike.

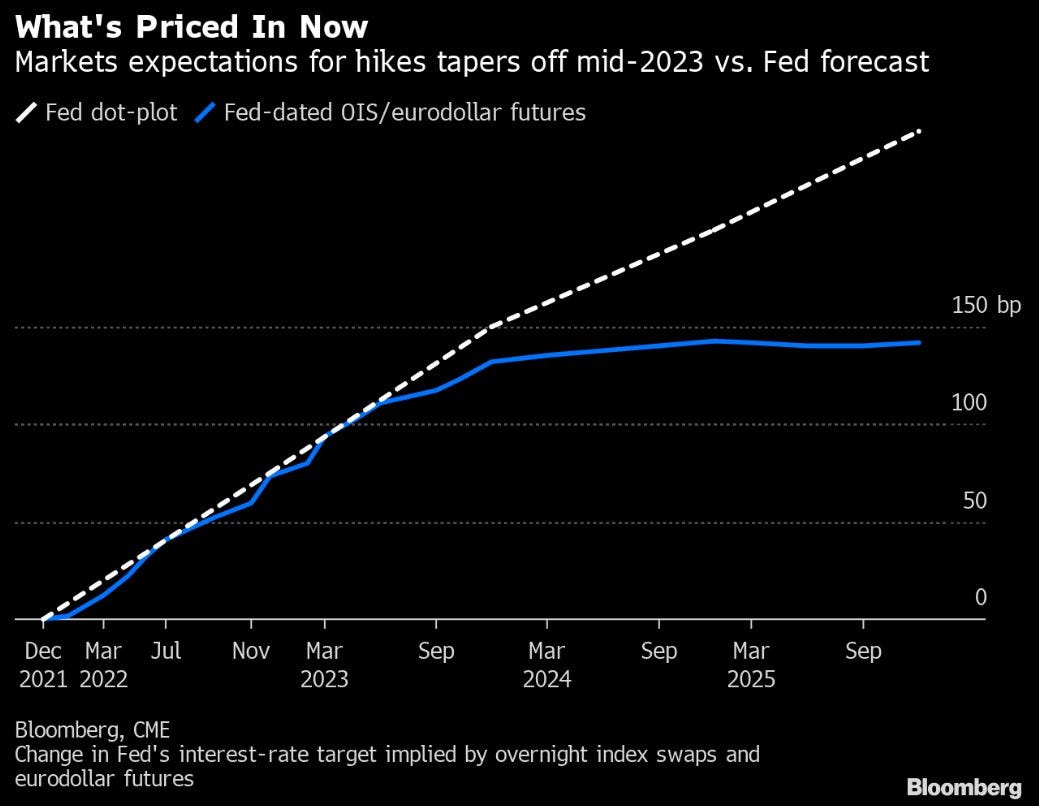

Why? Probably markets expected a more aggressive approach from the Fed, but it is even possible that investors don’t really believe to the rate path indicated by the central bank, as you can deduct from futures market (see picture below).

Indeed many professionals believe that next recession will arrive in 2023 and 2024, and will force the central bank to be more accomodative.

After an initial good reaction, equities became more nervous, especially tech stocks.

Where to invest now?

The biggest question is always where to put your money.

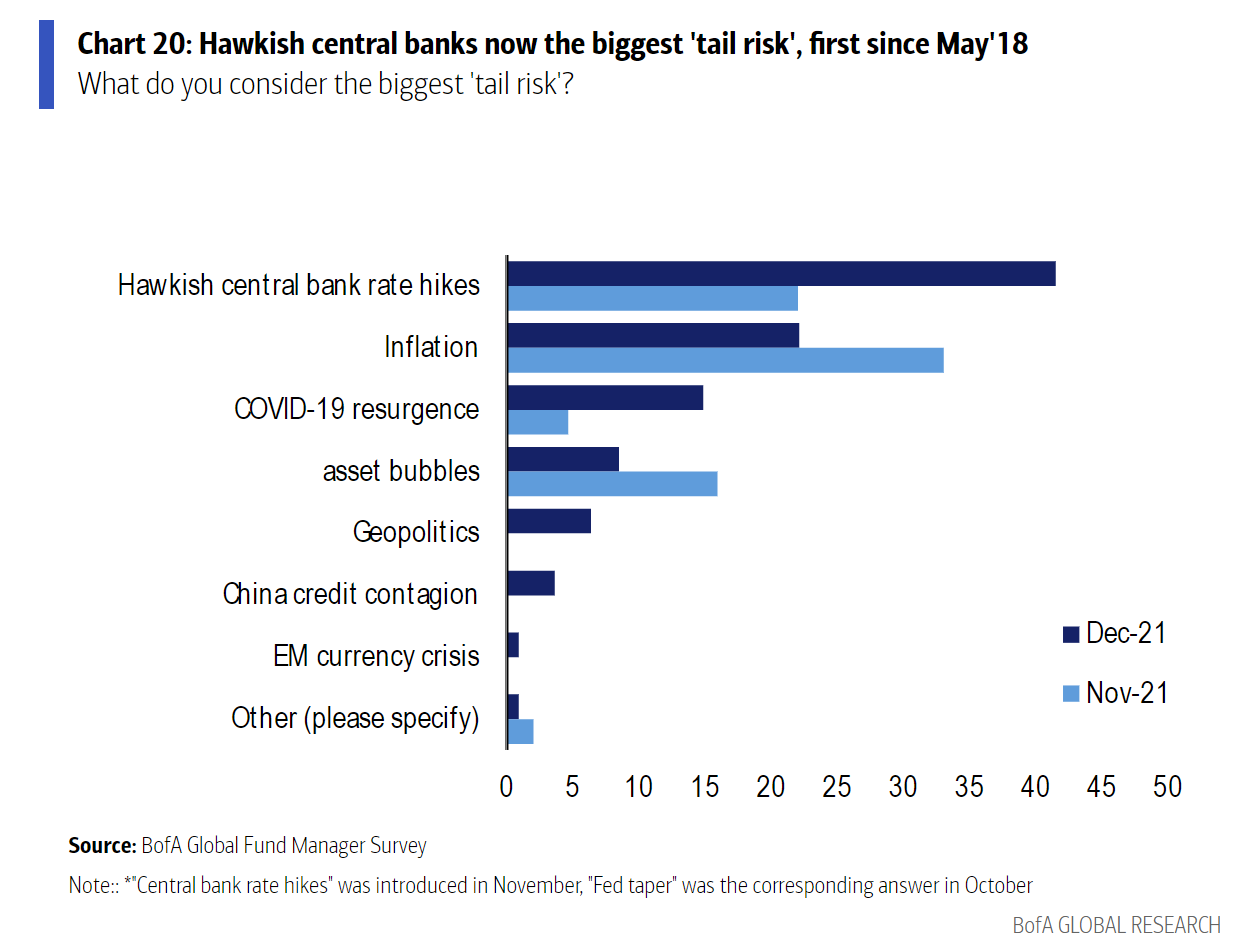

Let’s start by giving a look to the monthly fund manager survey by BofA.

It is interesting to see that now rate hikes are the biggest fear of investors, even more than inflation. Covid is again a source of concern (as cases are growing).

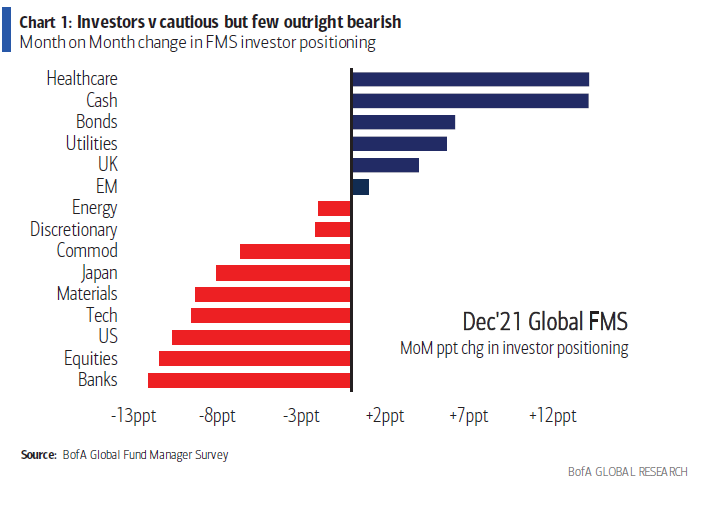

Moreover investors decided to reduce their equity exposure and to boost cash. This is a sign of more uncertainty and growing fears.

Should you be scared as an investor?

My answer is: not too much! It could be time to stay more defensive and raise some cash, but I still see bonds as a not attractive area, and equities as a better place to be, at least for the next few months.

As even suggested by Emmanuel Cau (Barclays), rate hikes and less liquidity don’t end bull markets, but they can add volatility and bring to less speculative valuations.

I already suggested few weeks ago to have a limited exposure to pure growth stocks, that had frothy valuations and my idea is still the same: growth and tech stocks can suffer more.

I think it is better to stay very diversified from several point of views, like geography, sectors etc.

My suggestion to stay diversified comes even from the potential impact of Omicron mutation on global economy. It will probably not have a very high impact, but several countries are already imposing new restrictions, especially in Europe, and this can slow the economic recovery.

Currently I would NOT push on the following sectors: Tech (frothy valuations for most of them), Travel & Leisure (Omicron will lead to less travel) and Energy (less travel means less oil demand).

On the other side I see as potentially interesting the following sectors: Financials (rising rates are good for bank balance sheets), health care (time to stay defensive).

I currently see even one more interesting asset: USD.

In 2021 Dollar has been king (up almost 7% YTD).

Can this appreciation to continue? I think yes.

For example I think that EURUSD can still go down more.

Currently EUR/USD is in a flag after a massive dollar appreciation during the past months, but the difference reactions of the 2 central banks (Fed and ECB) could bring to further fall, even below 1.12. I am currently long USD.

Finally I think you should be ready for some more volatility, but use that as a friend: volatility offers you opportunity!

Remember: this is not a financial advice! Make your analysis before to make any investment!

Follow my Instagram page if you want to be always updated on markets.

Have a great weekend!

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.