Tech Giants are pushing up equities

The tech megacaps are driving markets to new highs

Hello guys,

I hope you are enjoying my articles and learning something new about markets and investments. Finance is a very complex world, and it requires lot of study and open-mindedness. Be always ready to enrich your knowledge.

If you like my work please share the blog with your friends.

July: usually a good month

July is typically a great month for equities: for example look at Nasdaq 100 on past years.

The tech index has been up each July for the last 13 years and this year is not looking different.

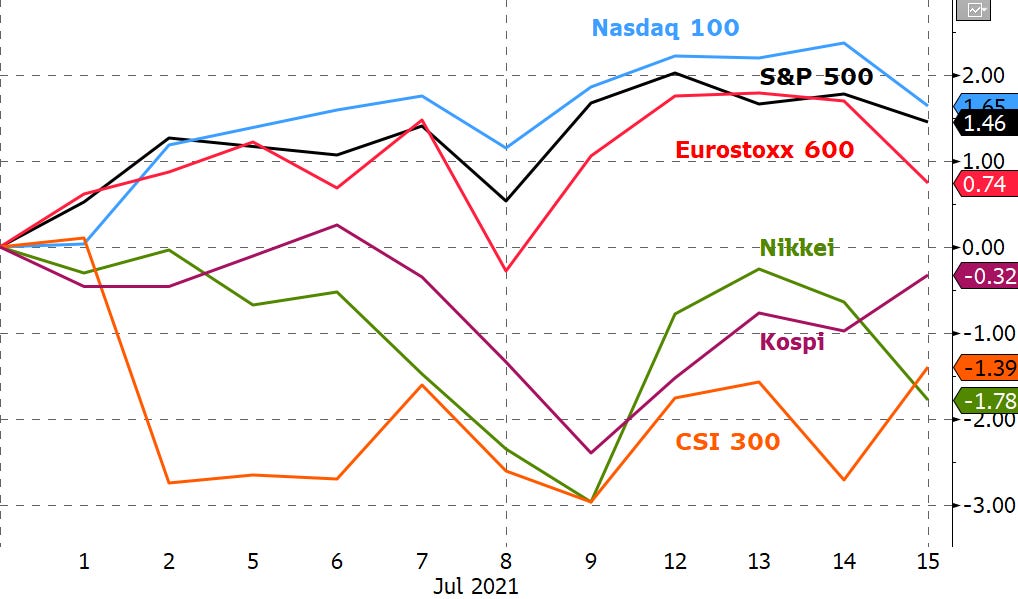

Here a recap of some of the principal global equity indices in July:

The performance of the indices has been taken on the closing price of 15th July. It is clear that U.S. stocks have taken again the lead and that tech and growth stocks are again on fire, while currently value stocks look weak.

Asian equities are still struggling to gain investors’ confidence, while Europe, after a great start of the year is going quite flat.

What’s wrong?

If we look deeper in U.S. indices we can understand what is driving higher the markets:

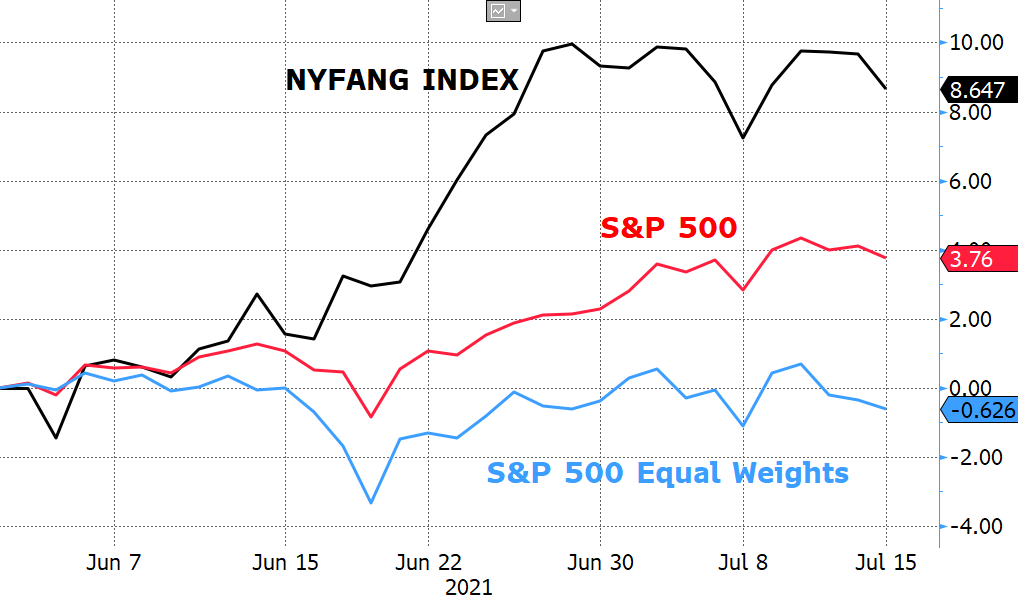

The answer is FAAMG, Tech Giants, or NYSE FANG+ Index in this case. Just to give you a quick introduction, the index is composed by only 10 stocks:

The index should represent a segment of the tech and consumer discretionary sectors consisting of highly-traded growth stocks of tech and tech-enabled company (but where is Microsoft?).

The most interesting thing is to see the divergence of performance, from the beginning of June, of the S&P 500 with the S&P 500 equal weights and the FANG+ index: it is immediately clear that the biggest part of the upside of the last 45 days is attributable to the tech giants. All other sectors are having lot of problem to give positive returns to the investors. Especially the energy sector is having the worst month, relative to S&P 500, since September 2020.

Biggest fears

What is driving this big divergence between tech giants and the rest of the markets?

The answer is not easy but there are several possible reasons:

- Delta variant: The number of new cases are increasing in many european countries to worrying levels (and you can see an inversion even in U.S.). The number of deaths and hospitalizations is still very low, but investors are starting to consider Covid as a primary risk again.

One of the main reasons why European equities and cyclical stocks had a great first half of the year was the reopening of the economies: the diffusion of vaccine and the return to normal business activity fueled most of traditional sectors.

Now the fear of new possible restrictions due to delta variant is again making investors confused: will the oil consumption go down again? Will the people stop to travel? Those are all legitimate questions. Autumn is coming and more information will arrive soon.

Meanwhile the “pandemic winners” (mainly tech and growth stocks) are back in fashion. Investors likely decided to put their money in some place that could work has an hedge in case of more concerns about Covid.

- Inflation: this remains the fear number one of investment managers. During last week CPI data were reported and once again they exceeded expectations. Month after month is becoming more and more difficult for the FED to convince markets about the “transitory” nature of the current inflation. In any case, few data can still be supportive of the transitory narrative.

As you can see in the above picture, used cars, vehicle insurance and lodging away from home remain the biggest components of the inflation spike, and they should go back to normality soon (especially the used cars once the bottleneck on chip will be resolved). Investors are probably embracing the thesis of the FED. For that reason the reaction to CPI data has been tepid and the 10 yrs Treasury yields continued to go down (now at 1.30%).

What now?

The two “factors” above mentioned have consequences on markets and you should think if you have to make some change to your portfolio.

The low rates and the tons of liquidity are making very hard to buy bonds, so equities remain the first choice of investments, but now the reflation trade seems a bit compromised.

Tech megacaps look like a safe heaven, and I would not stay away from those stocks, even if the current rally could be close to an end. In the long run they are still winners in case of restrictions or not.

The biggest potential losers if new restriction will be applied could be airlines, hotels and all stocks strictly related to entertainment. Even if vaccine will do its job, those sectors could suffer (people can just be scared to travel or go to the disco).

I still see industrials as an interesting sector since new infrastructure plans have been presented all over the world and governments are ready to spend more money to support real economy.

Moreover U.S. could be the best place for equities right now. Europe is facing big covid outbreaks and that can weight on investors sentiment.

An equity correction could arrive soon, markets look weak (breadth sharply declining), but I honestly don’t see concrete reasons to fear a bear market now, so I would still use any big drawdown to buy more quality stocks.

Finally, the earnings season just started: be careful if you like to bet on earnings reports, good results could not be enough to push stocks higher. In Q1 we already saw cold reactions to impressive results.

Have a great week!

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.