September is over, rotation is back

A spike on yields is changing the macro picture

Hello Guys,

Welcome back to “All eyes on Markets”.

Thank you to all the subscribers: we are now more than 700!

If you haven’t subscribed yet, do it now!

Now let’s see what is happening on markets.

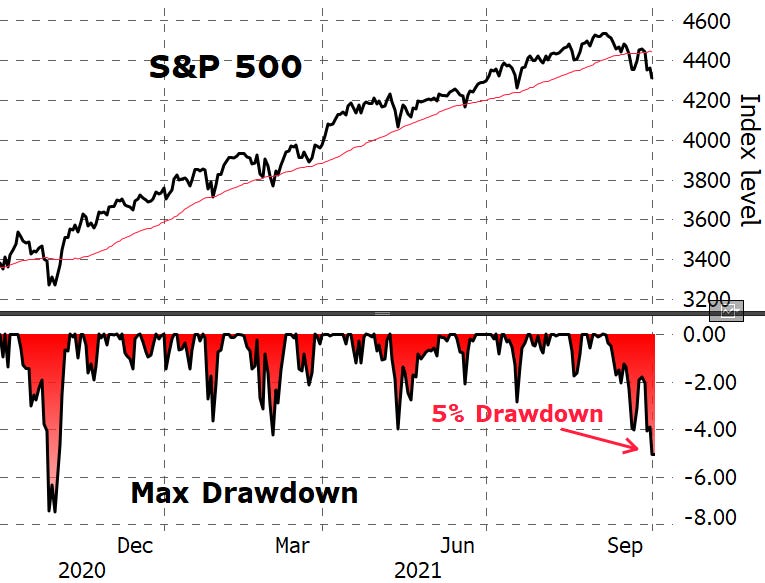

Weak September

September is over, and it has been a tough month, both for bond and equities.

Most of the global equity indices closed the month with a negative performance:

Seasonality has always been weak in September, statistically one of the worst months of the year for stocks.

We even saw a 5% drawdown on S&P 500 after a winning streak of 227 trading days.

In any case, the performance for the year is still positive for all the American and European markets, not for Asian ones, still hammered by China.

The yield spike

The month has been plenty of events, from Evergrande to the central banks meetings, and they put lot of pressures on markets, that are now more confused on what’s coming next.

Especially on the central banks side, the days after the Fed Meeting have been very interesting to look. The first reaction to the Powell’s speech has been “indifference”, even if the dot plot showed a mounting pressure on rate hikes.

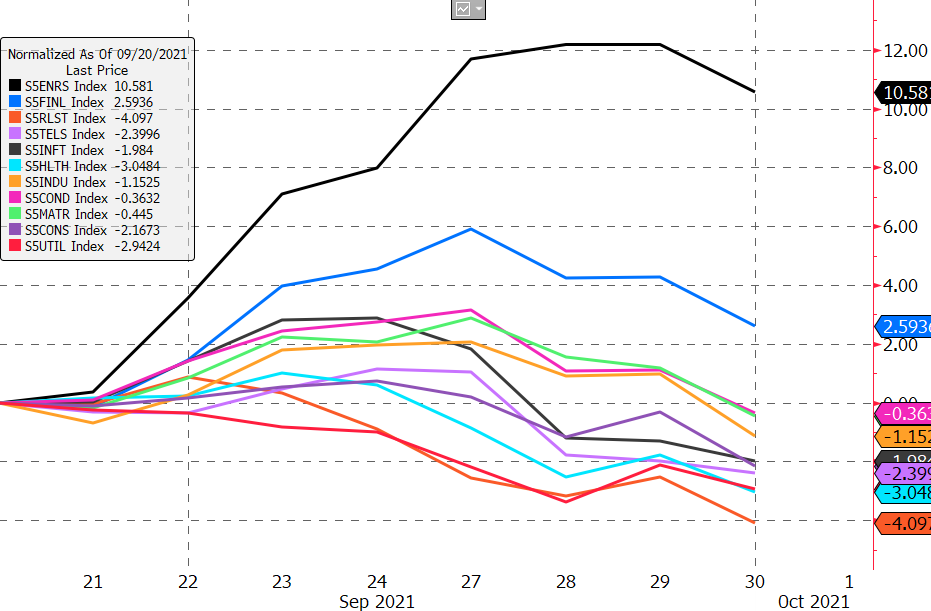

Just a couple of days after that, there has been a first big spike on the 10-Year Treasury Yield, that went from 1.30% to 1.42% (12 bps is a very big movement).

As I have told you already in the last two newsletters, it is very important to costantly monitor the Treasury because it can affect severely the performance of the other asset classes. Just look at the reaction of every sector since the yield spike (approximately on the 21 Sep 2021).

As you can see above, there are some beneficiaries from rising yields: sectors like energy, financials, materials and industrials can be winners in this environment, while tech, communication, and utilities can suffer.

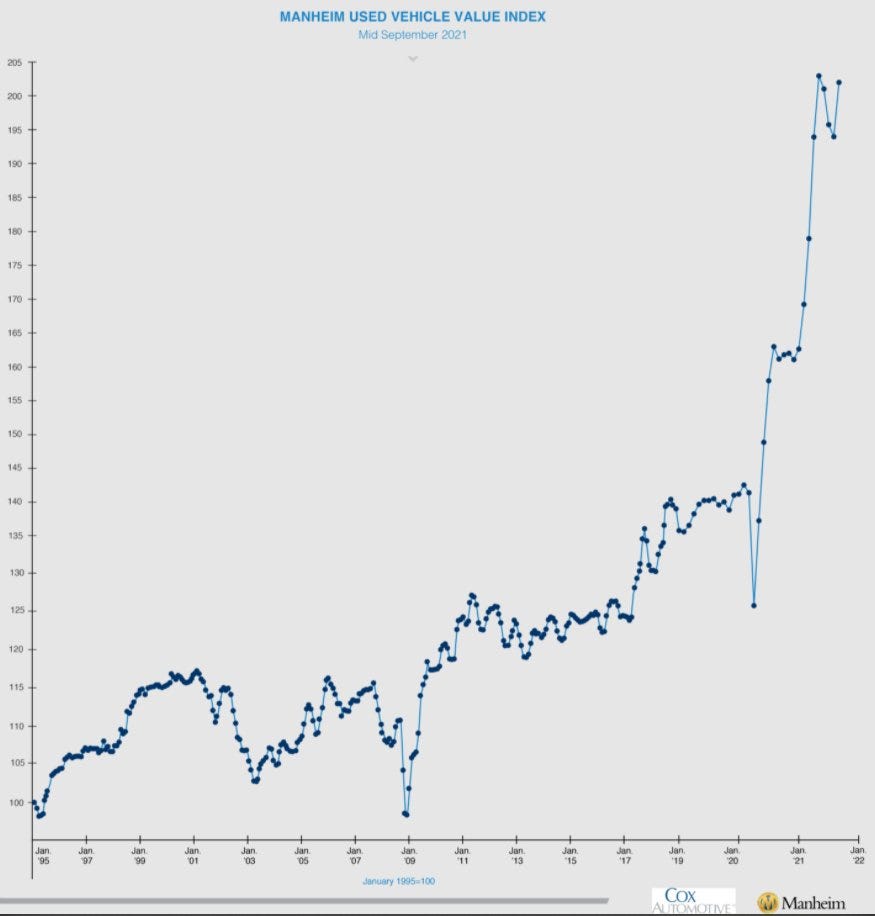

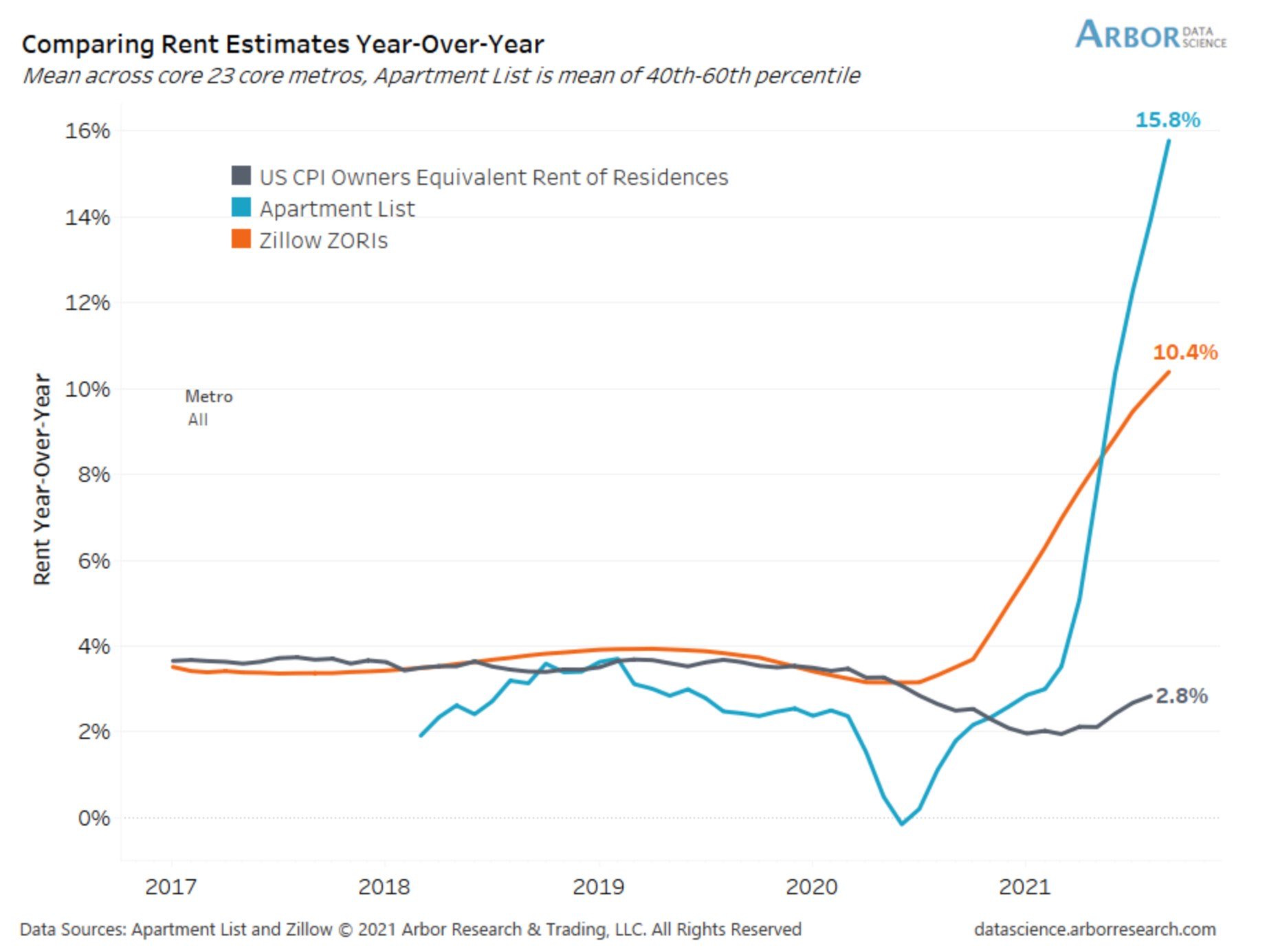

Inflation: less transitory than expected?

The last CPI release gave relief to the markets because it indicated a cooling in core inflation, but now some data, and even Fed Chair Powell are making investors more doubtful.

For example, look at the used cars price: after a break in August they are rising again,

Even the rents signal an upcoming rise in prices, as highlighted by Zillow and Apartmentlist.

Moreover Powell, during a panel discussion hosted by the ECB, this week, said that “It’s also frustrating to see the bottlenecks and supply chain problems not getting better — in fact at the margins apparently getting a little bit worse,” and even “We see that continuing into next year probably, and holding up inflation longer than we had thought.” (Source: CNBC)

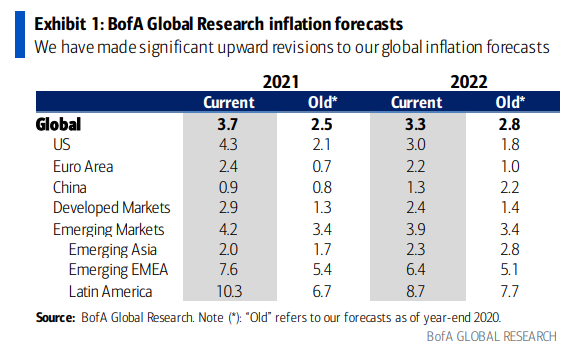

Lastly, BofA just updated its inflation estimates: the bank updgraded its view on every global region, but mainly in U.S.

The result of this inflation fear could be a return to the reflation trade.

Where to invest now?

A rising inflation environment, together with a slower economic growth, is a tricky situation for investors. First of all look at the correlation between stocks and bonds:

The two asset classes are now positively and even highly correlated. Why this can be an issue? Historically bonds have been a way to diversify investments and reduce the portfolio risk, but currently it wouldn’t work.

If yields will go up and the S&P 500 is positively correlated with bonds we should try to make returns in an alternative way, and try to invest on some specific sector.

Usually, in reflationary periods there are heavy sector rotations, as we saw in the last week of September and in February and March of this year. So we could try to be more defensive by allocating more on sectors like financials, energy and generally value stocks.

One possible idea could be to increase the exposure to the Dow Jones, tipically a more value index. Another idea could be to go long on Russell 2000, since the small caps tend to be more cyclical.

On the other side, the Nasdaq doesn’t seem the place to be, better to stay conservative there.

Those kind of rotations can last few weeks or few months, difficult to say, but can be painful if you are on the wrong side.

Another idea could be to buy an ETF Short or Ultrashort on 20-Year Treasury (TBF or TBT).

Of course this is only my personal view on the base of last market events, and not a financial advice.

Have a great weekend!

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.