Markets need a new catalyst to start a new rally

All eyes on earnings

Hello Guys,

Thanks to all of you, we are now more than 820!

If you have any friend interested in finance and investments, please tell him to subscribe.

Time to look at the last market developments.

Lot of noise, but markets flat

I often read about stocks going “to the moon” and “stonks only go up”, and they actually did it in the last year, but what about last 3 months?

Let’s see a chart on the main global and american equity indices:

Not lot of growth, Right?

As you can see above, most of the indices are little moved in the last 3 months.

The StoxxEurope 600 has been the best performer.

In U.S. the S&P 500 and the Nasdaq gained 1.7%, while the Russell 2000 has been the real winner: it increased by almost 4%.

This scenario can be frustrating for an investor: lot of time without seeing notable gains, but this is normality for markets. They always need a “consolidation period” after big rallies, and often consolidation means correction. So far we just watched a small drawdown (5%), so nothing special. We have been quite lucky.

Now the question is: what can drive markets up?

My answer is: earnings!

A new earnings season

On Wednesday JP Morgan has been the first large cap to report its Q3 earnings, followed by all the others major banks, like Goldman Sachs, BofA, Citigroup and Morgan Stanley.

This earning season is very important: investors are looking for an indication on the current status and perspectives of the economy.

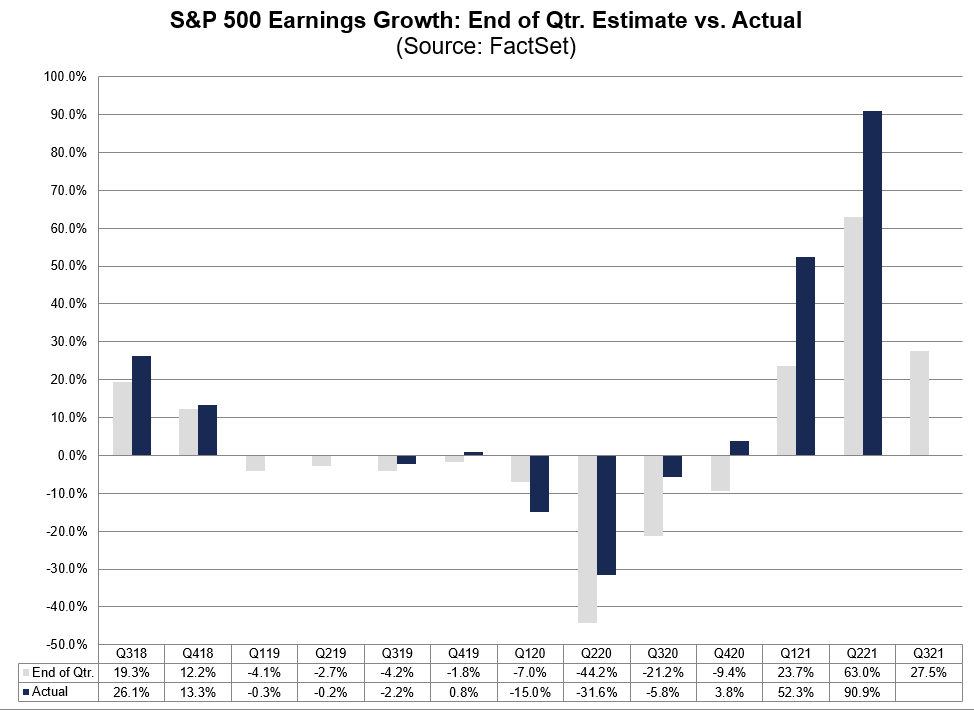

Can earnings continue to grow at a reasonable rate?

Analysts are expecting a 28% earnings increase YOY, much lower than Q2:

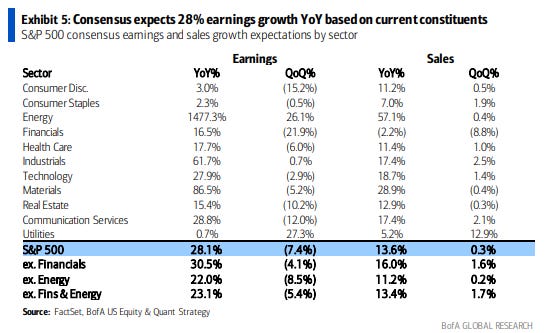

Furthermore, energy, materials and industrials are the sectors where the analysts see the highest growth:

Utilities remains the most hated sector, and even the worst performer so far.

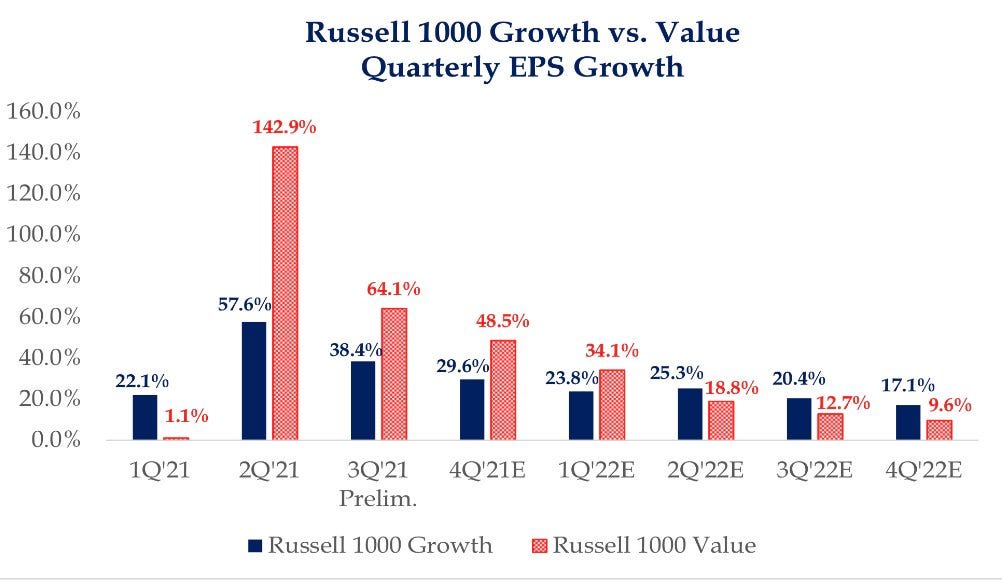

Value stocks is the area where there are the biggest expectations, compared to growth:

From the last chart you can understand why many strategists see a sector rotation for the next few months: value stocks are expected to make the biggest jump on earnings, before to be surpassed again by more “performing” companies (tipically growth stocks).

So far financials released good results, better than estimates on revenue (sales growth YOY 8%) and earnings (net income growth YOY +43%).

Markets have been quite flat and they need a new catalyst to start a new upward leg. Good earnings can be the most obvious reason for investors to maintain a bullish view on equities. There is even a good link between the S&P 500 performance and the forward EPS.

High inflation, no fear

The monthly CPI was the most awaited macro data of week, and it surprised to the upside. It came slightly higher than expected (+0.4% vs +0.3%), but mainly due to the food component. The CPI ex food & energy was in line with expectations. (+0.2% vs +0.2%).

Markets reacted in an unexpected way: Treasury yields fell, USD depreciated and tech stocks overperformed the others.

Why? Not easy to say, but maybe this was a “sell on news”, or maybe the data were below the real markets expectations.

Does this data change the future picture? I don’t think so!

As written even in the FED minutes, the Fed will start to taper by mid-November or mid-December. The focus is now on rate hikes. Markets expect the first hike by November 2022.

New data on inflation and job market will change expectations on rate hike timing.

Where to invest?

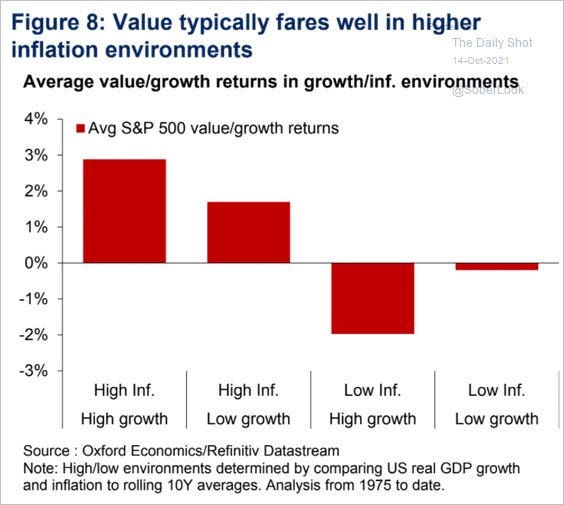

The new macro data do not change the market outlook: bonds and cash do not seem the place to be!

Equities and commodities remain the most interesting asset class. My preference is still for cyclical sectors (value stocks) and small cap (Russell 2000).

Russell 2000, the most known index on small cap, is interesting even from a technical point of view. After 8 months of horizontal price movements it looks in a good position to test again the all-time highs. The 200 days MA seems a good support, together with the upward trendline. The investment is appealing and with a balanced risk.

Moreover in the last week I wrote that I have a short position on Treasury (through TBF Etf). I am closely watching the performance of the Treasury Yield: in case it will go below 1.50%, I will evaluate if take some profits.

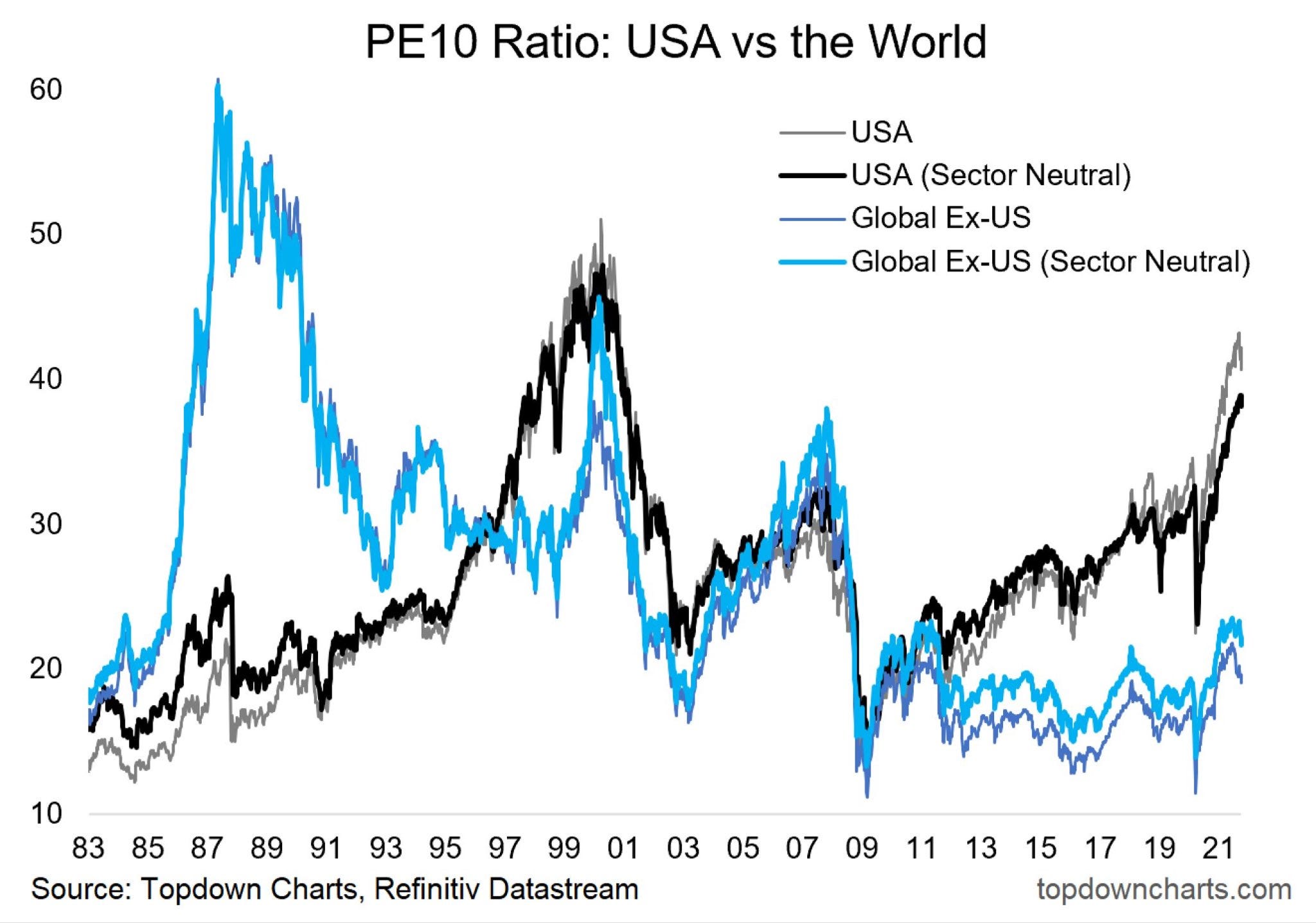

Finally, I still want to stress the interesting evaluation of the stocks outside the U.S. (like Europe).

The gap of the PE ratio between US and non-US stocks is very high, and foreign stocks tend to outperform U.S. when cyclicals are strong. Maybe here there is the potential for a catch-up trade.

Make your studies before to put your money in any financial instrument.

Have a nice weekend,

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.