Low inflation can be good for equities

Low inflation can be good for equities

Last CPI data may have calmed markets

Hello guys,

I hope you are all having good time.

In case you are reading this article but you haven’t subscribed yet, do it now!

September is typically a weak month for equities, especially in the second half. This year doesn’t seem different and indices are performing poorly in September as well.

So far lot equity indices are negative MTD, especially in U.S. and Europe. Japan is the hottest spot right now, with a solid performance in September (+7.9%).

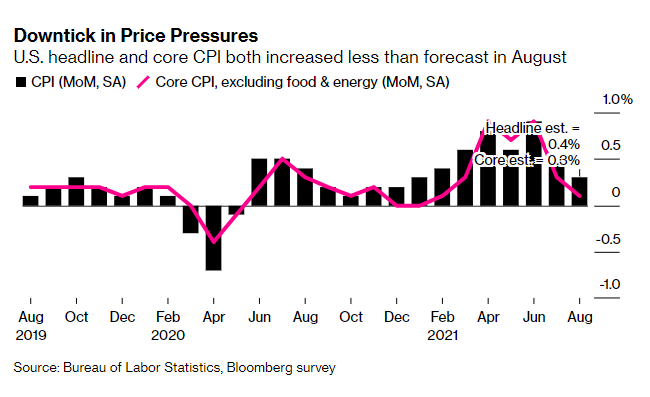

Markets are having a “break”, but there are even good news, especially from the last U.S. CPI release, lower than expected. Looking at the trend of the inflation in U.S. it can be noted that the “transitory” story, highly sponsored by the FED, is materializing.

In August, Core CPI (ex Food and Energy) has been +0.1% (vs estimates of 0.3%), signaling a slowdown. Let’s give a look at all the categories included in the CPI:

The price of used cars finally started to go down (and it will go down more in the next months, as soon as the new cars production will ramp up). Moreover airline fares had the biggest monthly decrease (-9.1%).

The weak data reassured investors one more time: no need to accelerate tapering and rate hikes! This could maintain yields low and sustain equity valuations, especially on tech & growth stocks.

What are the new risks?

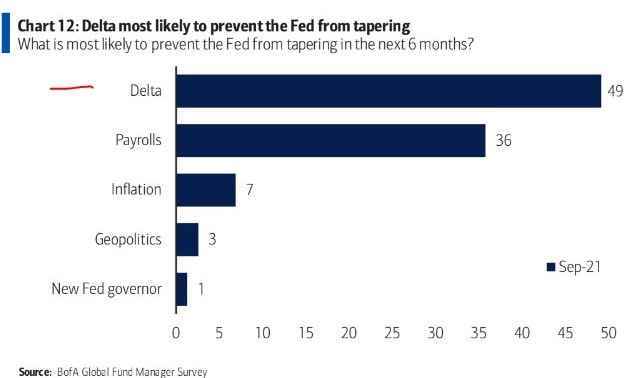

As usual Covid remains one of the biggest threats to the economy, but so far the pandemic developments are not bad. In any case, investors still believe that Delta variant is the main reason why FED could not begin tapering in the next six months.

If we look forward there are other themes that could create concerns on equity valuations: for example in U.S. the Biden administration is trying to pursue a raise in corporate taxes. That raise will impact negatively on EPS, and on company valuations, at least in the near term. One main point could be how big the tax increase will be. Markets price a 62% of probability to see a corporate tax increase:

Another interesting point regards Europe and its energy supply. Recently the price of the natural gas had a huge increase, and the commodity is now up more than 100% YTD. Europe is highly dependent on gas (especially from Russia), and now it has 2 issues:

The increase in gas price could affect companies margins (companies will spend more for energy, eroding their profits) and consumers.

Supply shortage if the inventories will not be enough to cover any potential supply reduction from Russia.

Of course a persistent spike in energy costs will reduce EPS estimate for european stocks, at least for 2021. Markets are not still worried about that, but look at the situation closely.

Any investment idea?

Last week I mentioned some interesting region where you can invest (and I didn’t changed my mind). Today I would like to focus on other factors:

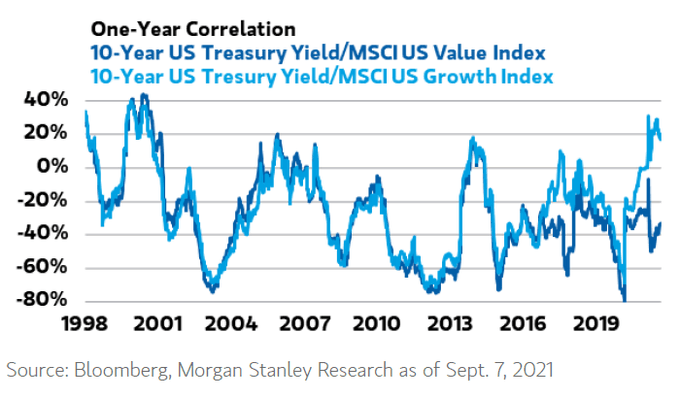

Value vs growth: as long as Treasury yield stay low, growth stocks can continue to benefit and attract money from investors.

The correlation between Growth and Treasury Yield is still deeply negative, while the one between Value and Treasury yield is very positive.

What can it mean for your investments?

If you think that the yield of the 10-Year Treasury will stay low, it could be good to stay long on tech and growth stocks (a Nasdaq ETF for example). On the contrary, rising yield should make you think if it could be better to put some money on value stocks (and maybe indices like Dow Jones or Msci Value).

Oil stocks: not only natural gas prices are up. Oil prices are surging again. Why?

The impact of hurricane Ida is weighing on U.S. Oil Production, as many productive sites are still not working.

Oil demand remains sustained, but on supply side there are more constraints now. The result is higher oil prices.

The main point behind a long call on oil stocks is that there is still a huge gap between oil prices and stocks of oil producers, especially in Europe.

There is the potential for a good catch-up trade here.

Have a great weekend!

Bye

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.