Half Year is gone. What's next?

From fear to euphoria

Welcome back on “All Eyes on Markets” by Market Radar. I am very happy to see that lot of people are subscribing to the newsletter. We are creating a great community on finance & investments.

If you have other people potentially interested, just invite them to join the newsletter!

So far 2021 has been a year full of events: especially, vaccination campaign started all over the world and we finally have the opportunity to think to a post-covid world, even if recently the Delta variant is creating some worries.

The focus of investors shifted from Covid to the economic growth and the rise in inflation: a vertically increase of the price of almost every commodity , a bottleneck on supplies and a big rise of price for rents, used cars and other goods brought to a spike in inflation. Investors are still asking themselves if it is “transitory " or not. That could have a big impact on every asset class.

From mid-February a big correction on bonds started, and the Treasury yield went up from 1.15% to 1.70% before to calm down. The impact was big on equities too: the sectors positively correlated with inflation (ie. value stocks, commodities, miners, financials, industrials) had good times, while many of the pandemic winners (mainly growth stocks) saw big drawdowns.

Since the last FED meeting and the release of weak jobs data, growth stocks started to overperforming again and the gap with value has been almost entirely filled.

Let’s see some charts!

Here a recap of the performance of the most important equity indices:

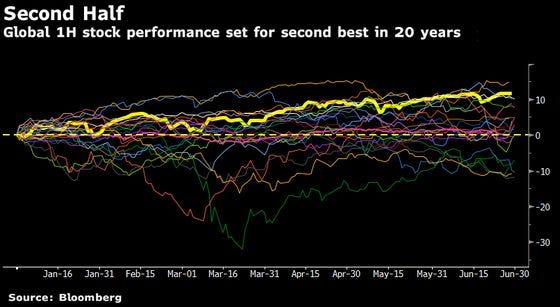

As you can see above U.S., Europe and South Korea have been the best performers, while China and Japan had a tepid first half (despite a strong start of the year). This year global equities had the second best H1 in the last 20 years (see the chart below)

Energy has been the best sector, while utilities the worst:

In U.S., Marathon Oil has been the best stock of the S&P 500, Viatris the worst. See below the details of the best & worst performers.

We can see the same recap even for the Eurostoxx 600 components, where Future Plc has been the winner:

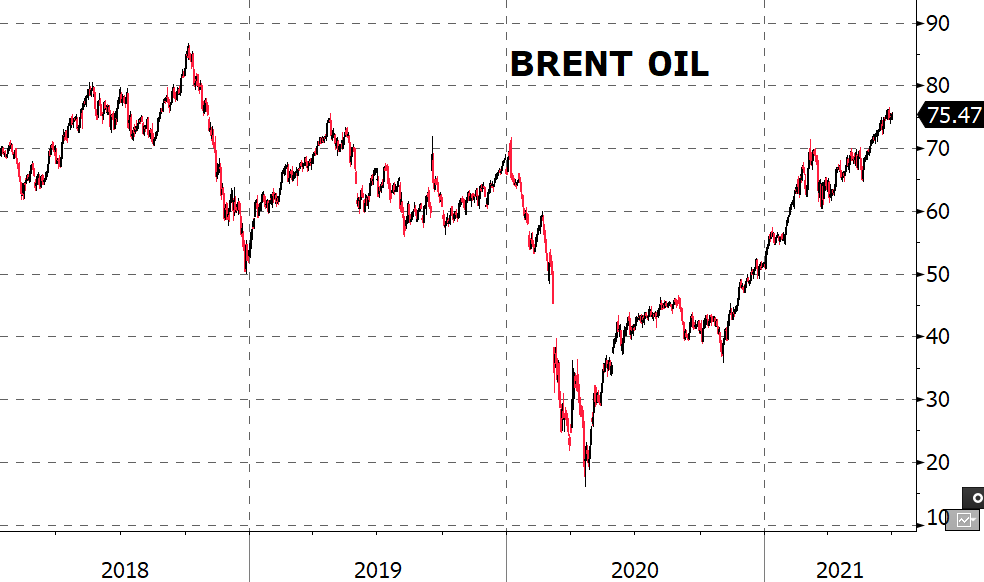

Meanwhile oil price is at its highest level since 2018. How long can it go up? The upcoming OPEC+ meeting will be decisive for sure: the coalition, led by Saudi Arabia and Russia, is considering if to increase oil production and ease the current price pressure.

Finally, we cannot overlook cryptocurrencies. Bitcoin had an incredible run until the beginning of May, before to start a furious correction: the price has halved from 60k to 30k. The performance YTD is close to +20%.

Other crypto had unbelievable returns: ETH +185%, XRP +175%, DOGE +5,000%.

WHAT NOW?

Past is past and I hope that everybody made good gains in the first six months of the year, but now we should think to the possible market scenarios for the rest of the year.

Probably the main themes will be the following:

1- Central bank moves: investors will closely look at inflation and jobs data in US. If both will be higher than expected (higher inflation and higher employment) more and more people will believe that the FED will start the tapering and the rate hikes before than currently expected by markets.

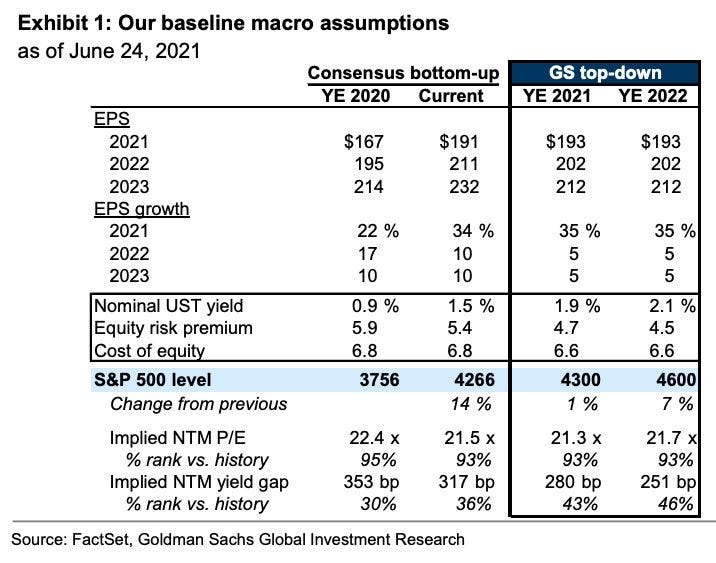

Probably the primary effect will be a rise of the Treasury Yield as inflation expectations will put pressure on that. Goldman Sachs is forecasting a 10 Yr Treasury Yield for the end of the year at 1.90% (look at “Nominal UST Yield” in the table below). Today it is at 1.46%.

2- Covid Delta Variant: even if we are becoming confident that pandemic is over, this is not the truth and we cannot underestimate the risk. In developed countries the administration of vaccines is going well and the herd immunity seems possible in few months.

The main risks related to Covid are the following:

vaccine campaign in poor countries is still behind. Remember that as long as the virus continue to be transmitted, the risk of new variants is very high.

the herd immunity could not be reached: for example, in US after a super start now the daily vaccine rate is going down sharply. The number of first doses is still not enough to reach the immunity.

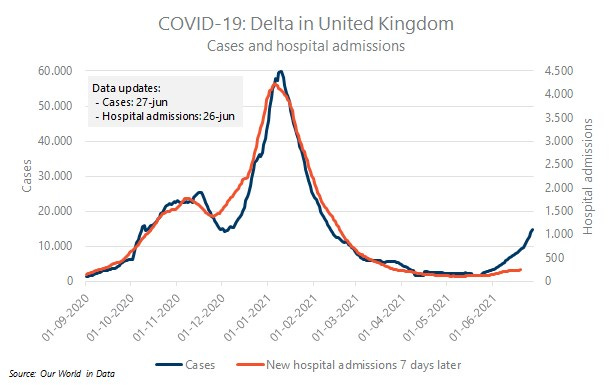

Delta variant: in UK there are more than 20,000 cases per day and it hadn't happened for months. The most interesting and even the most promising statistic is the one regarding the hospital admissions, that are not going up, thank to vaccines that are doing their job.

Source: Our World in Data

The 2 risks above mentioned can drive markets in 2 different directions. If the Delta variant will start to be a real issue, the fear of new lockdown will bring down again value stocks, cyclical stocks, commodities and the 10 year Treasury yield, and it will boost all the tech stocks.

Instead the scenario with rising (and permanent) inflation (and economy fully open) will have an opposite effect on markets.

Many of the most known strategists of Wall Street are currently not scared from Delta Variant: for example, Marko Kolanovic (JP Morgan) just wrote a note where he reiterated his call long on Value and Cyclical stocks. He said that the current market positioning is not justified (June has been very bad for value) and he sees markets in a setup similar to February (when a variant, known as B.1.1.7 came out): “When the market properly assessed the risk of B.1.1.7, yields and value staged a strong rally from mid-February to mid-March, while growth stocks (often perceived as beneficiaries of lockdowns) sold off”. “There is a similar setup now with the so-called Delta Covid-19 variant fears”.

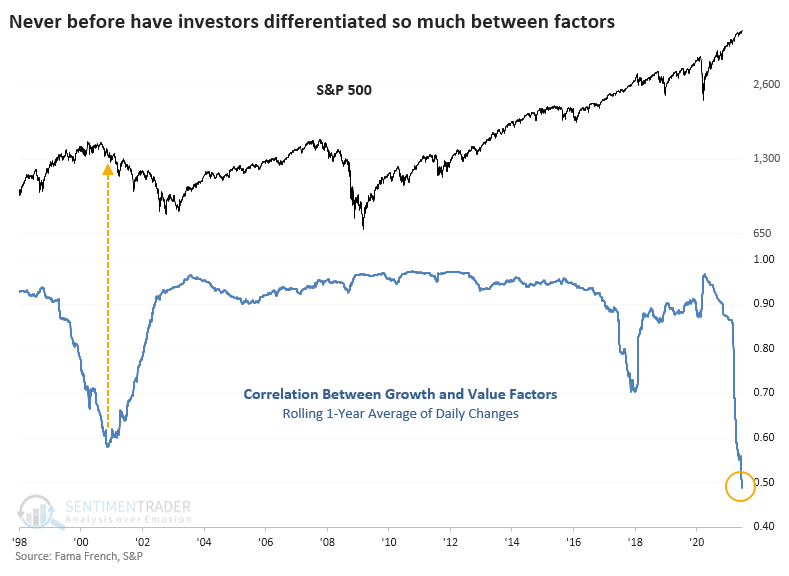

Finally, let’s see these 2 charts, about correlations:

Correlation between tech stocks and 10 yr Treasury yield is now negative: it means that if Treasury yield goes up, tech stocks will go down.

Secondly, correlation between value and growth stocks is very low, as it is never been in the last 20 years. That means that positioning is becoming very relevant, and if you choose the wrong side of the markets, your portfolio could suffer a lot (or at least underperform)

My view currently is close to the consensus: I don’t see Delta variant as a big issue right now but it has to be monitored closely, in order to understand its potential effects on real economy and markets. It is not good to be taken aback!

I see bond yields to go up, so I am not excited to hold any bond (infact I bought the TBF ETF), even considering that spreads on corporate bonds are very low. Instead I am still moderately positive on stocks as long as there are not big alternatives and I embrace the value rotation and short duration view (but not totally), so I will try to use the pullback to buy more cyclicals. Europe looks more attractive than U.S., even if the S&P 500 has been the real winner so far. The most famous index beat both Nasdaq and Dow Jones, probably because it is more diversified, but be ready to jump on one of the last two, as long as new data will arrive and I will update you with my view (that is NOT a financial advice).

Have a great weekend.

Market Radar

——————————————————————————————————————

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.