Fund positioning, Delta variant and China suggests caution

New risks for investors on the horizon

Hello Guys!

I hope you are fine!

If you haven’t subcribed to the newsletter yet, do it now!

Today I will talk about funds positioning and which are currently the biggest risks in the markets.

Positioning: Signs of fear

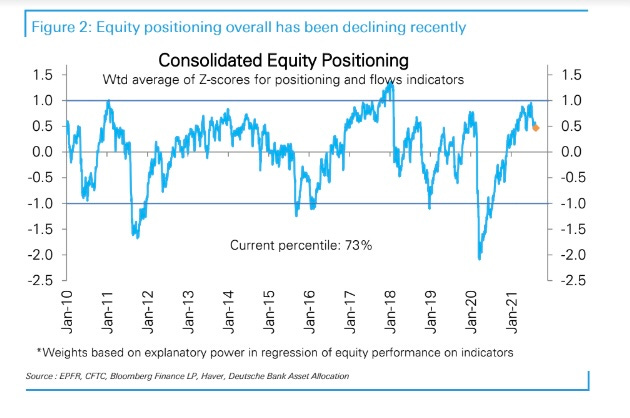

Several investment banks try to track and monitor the flows and the positioning of the investment funds, in order to understand were “smart money” are going(even if they proved not to be always so smart). In many cases the results of those research don’t go in the same direction, but the last data tell us uniquely the same story: funds are reducing their risk and their exposure to equity.

As shown in DB chart, above, it seems that the equity positioning of funds is going down from the extreme of July (97th percentile) to a softer level today (73th percentile).

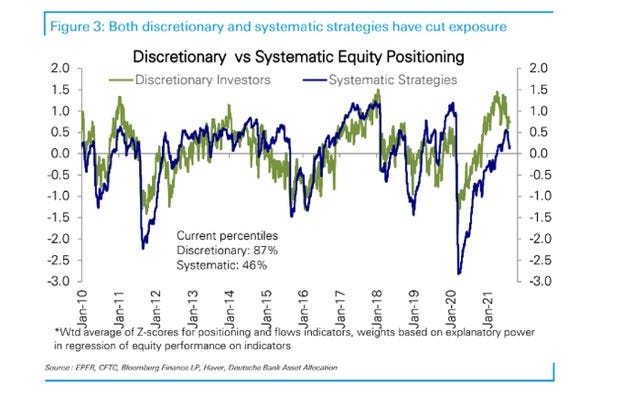

Both discretionary and systematic investors are reducing their exposure to equity, as you can see above. Especially systematic investors (let’s say algo driven) have an extremely light exposure.

But if they are selling equities, how is possible that equity indices are going up?

There could be several answers. One could be that retail investors are now a big part of trading volumes and they can absorb funds selling. On the other side it could be that funds are selling only selected parts of equity markets, as showed by DB in the chart below.

Here you can see that CTAs (Generally, a CTA fund is a hedge fund that uses futures contracts to achieve its investment objective, source: Investopedia) are mainly cutting exposure to Emerging Markets (China is included in emerging), Japan and Russel 2000, while they are still heavily into the S&P 500, Nasdaq and EU50.

It is possible that they are selling in the first place the riskiest part of the portfolio or maybe they see those areas as the weakest in the current markets environment.

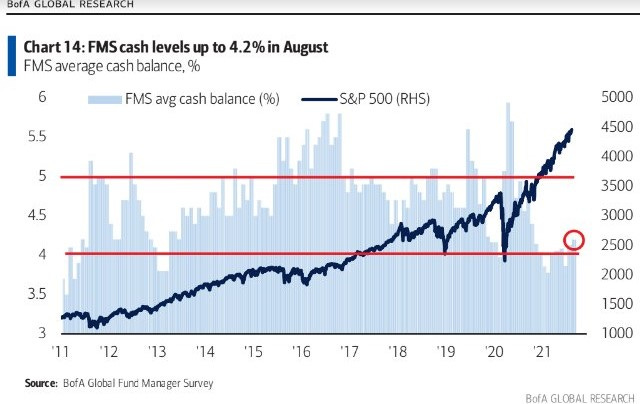

Other banks signal that investment funds are reducing their risk exposure. For example, Bank of America, in its monthly Fund Manager Survey highlights two interesting points.

The first one is that funds are increasing their cash level to the highest percentage of the year. Of course high cash level indicates a more conservative asset allocation.

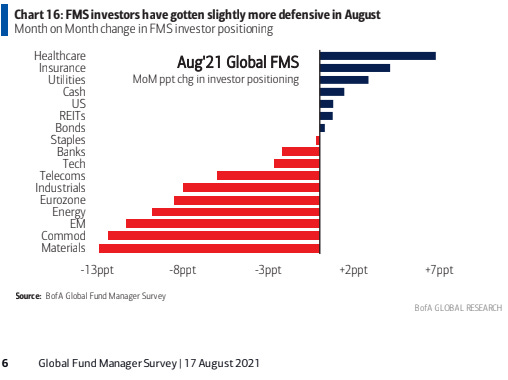

The second point is maybe the more interesting: in the last month fund managers reduced the weight of some sectors, especially materials, commodity, EM and Energy, all considered cyclicals and linked to an economic recovery, and they increased the positions in Healthcare, Utilities and Cash, all defensive sectors.

It is clear that they are rotating their portfolios to a more defensive positioning.

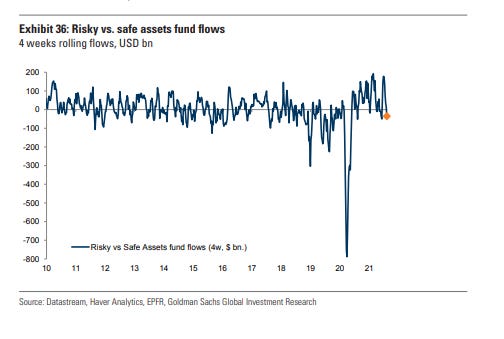

The last chart comes from Goldman Sachs and it shows that flows are going on safe assets instead of risky assets.

Why Fund Managers are more cautious?

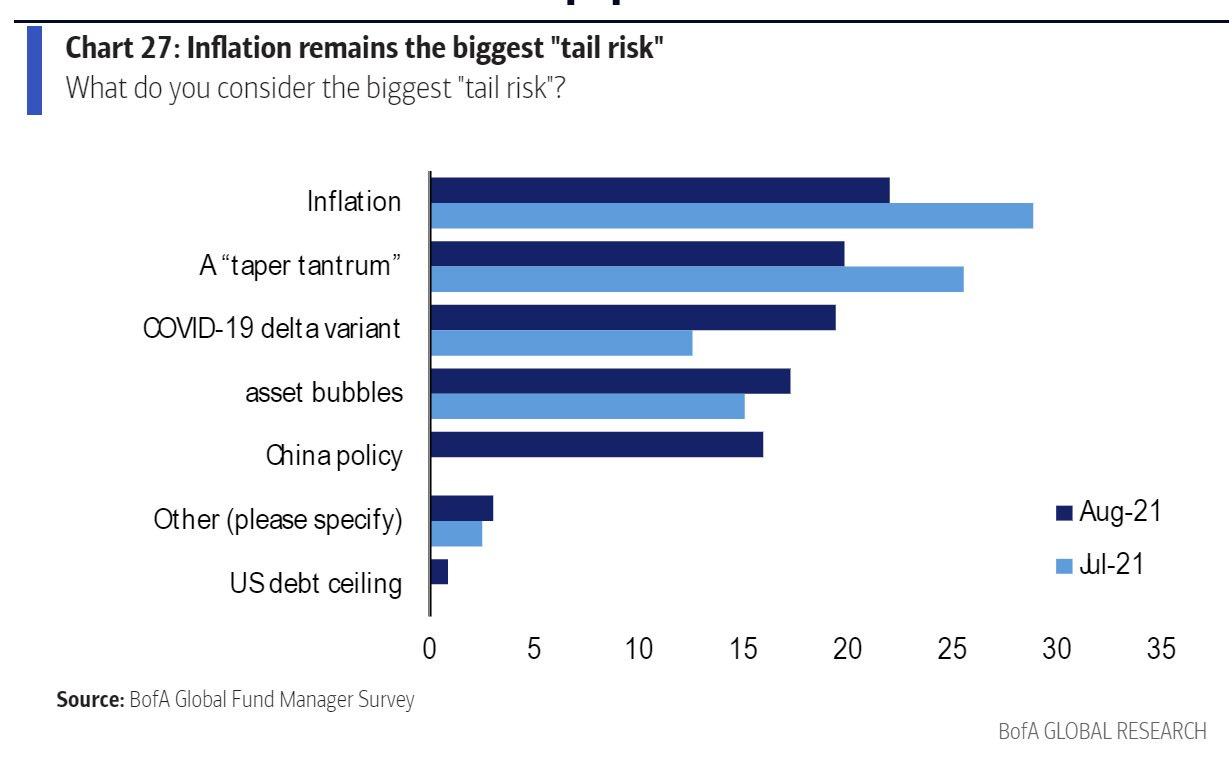

Let’s start from watching another part of the Fund Manager Survey related to the “tail risk”.

The main fear of investors is still inflation, but less than a month ago, and the same can be said for “taper tantrum”. The fears that increased most have been “Delta Variant” and “China policy”. I would focus the analysis on the last two points.

Markets are probably repricing the impact of Delta variant on the economy. Data regarding new cases and hospitalizations are rising again in U.S., and the last data on consumer confidence suggest that people are wary and less available to consume. Generally, all the U.S. economic data are coming lower than expected, and that could indicate that U.S. growth has peaked and now is slowing a bit more than what analysts believed. On this matter you can see that the Citi Economic Surprise Index has now turned negative.

In Europe the numbers regarding the new Covid wave are less worrisome, and hospitalizations remain very low for now. This is likely due to higher vaccine rate and to the fact that the vaccines have been administered later than U.S. and Israel (that are now going with the third shot).

As long as the data on Covid will continue to get worse, we will likely see markets to stay in kind of risk-off mode.

The other main risk factor is China: the CCP is continuing to hit big tech companies, with announcements of more and more regulation, and with some talks regarding economy inequality and the necessity to redistribute wealth. It seems that China’s stocks fall is not over yet, and CSI 300 index returned -8.5% YTD.

Moreover last data from China (like retail sales, industrial production, Caixin PMI) indicate a lower-than-expected growth ahead.

Finally the Covid situation in China is very difficult to understand: data regarding the vaccine efficacy and new cases are not clear, and this is another worrisome issue to deal with.

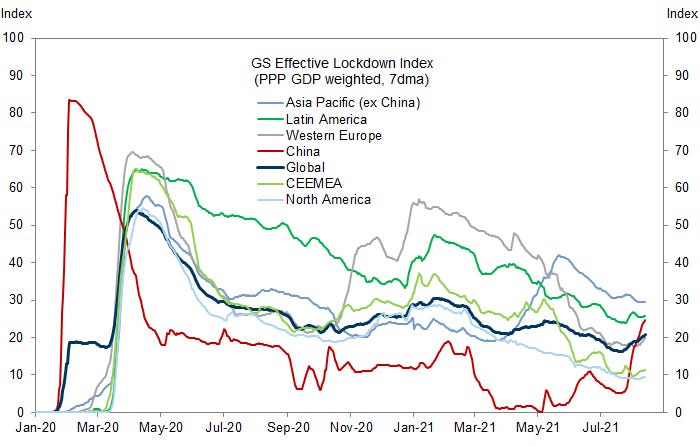

The chart from Goldman suggests that China is imposing some new restrictrions, that of course can impact on economic activity.

The sum of all the above points are making investors skepticals on China, and the result is that stocks are still decreasing sharply. Maybe it is time to give a look and an opportunity to some of those stocks…

What to expect next?

As long as the above mentioned fears remain, we could see a market correction and more flows to defensive assets and probably even growth stocks.

There is a good correlation between the relative performance of Growth vs Value and the new covid cases in U.S.: when cases go up growth stocks tend to overperform and vice versa.

Moreover you have to consider that equity indices in Europe (Stoxx 600) and U.S. (S&P 500) haven’t had a 5% drop in nearly 200 days (in Europe 130 days). So it would not very strange to see a correction.

Finally I think that now could be wise to have a limited exposure to equity, especially to value and cyclical stocks. All sectors linked to reopening and economic cycle could suffer for a while, and it would not be surprising to see tech stocks to overperform in the next days.

U.S. economic is in better shape than Europe, but valuations are much higher, and Covid in a worse trend: for those reasons I see Europe as a potential area of overperformance in the coming weeks.

In any case corrections are healthy and offer good entry points. Indeed I see the long-term picture for equities still positive and it could be reasonable to use any big fall to accumulate more stocks. I suggest to proceed step-by-step on new purchases: use any little fall to invest a small percentage of your liquidity, and don’t put all your money in one trade and in one day. Maybe you won’t take the lows, but this is almost impossible and not an investor duty.

Have a great weekend guys and leave below any comment you have.

I will be on vacation for a couple of weeks, so I will post less than usual. Time to recharge my batteries.

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.

I really enjoyed this analysis. Some great charts and perspectives. Thank you!