Hello Guys,

I hope you are great and making great gains!

If you haven’t subscribed yet, do it now!

This week has been plenty of events, from Evergrande crisis to the FED decision, but so far markets reacted well, and the dip didn’t last long.

Let’s see some interesting charts, useful for your investments.

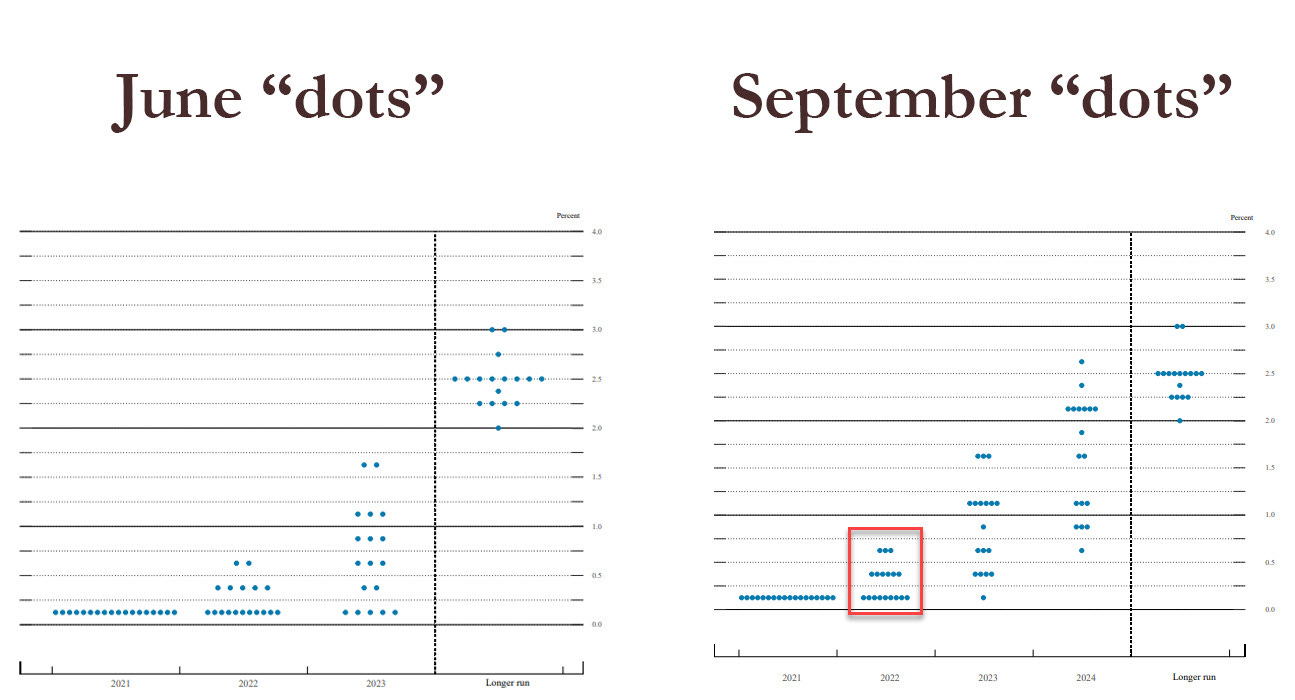

FED: Dot Plot signals a more hawkish Fed

In case you don’t know, the dot plot is a chart that shows the outlook for the federal funds rate. It is posted 4 times a year.

It is interesting to compare the last 2 “dots”: in September 9 members see rates to increase in 2022, while in June only 7 had that view. This means that more members are ready to accelerate the rate hike, scared of high inflation, and it is a clear hawkish signal.

So far equity markets reacted well to FED Decision and Powell Press Conference, but I think that too much good data could make investors to believe in a more aggressive policy from central banks, with all its consequence (like rising yield, value stocks to overperform, reflation trade to back in fashion).

Evergrande in trouble: be careful on China

The hottest theme of the week has been the Evergrande “almost default”. In case you want to read more about that, I suggest to read this article from FT (very interesting).

Goldman Sachs tried to calculate the potential impact on Chinese GDP of a crisis on property market. As you can see below the effects can be big.

The Chinese government will have to face the Evergrande crisis in the right way, if it want to avoid a systemic crisis (we just don’t want to see another Lehman!).

Moreover, this is just the last of a series of delicate decisions for China, like the regulation of tech companies and the regulation of the education sector. The issues are becoming numerous and China is showing signs of economic slowdown.

The slow down is clear in many areas like services, manufacturing and economic activity. All those factors suggest prudence with China and even with its main partners, that you can see below.

A less performing China could impact the performance of other countries, like Singapore and South Korea.

There are lot of Chinese companies that have attractive valuations, but it is better to be careful with investment in that geographic area, because volatility in the short term can be high. I think it is good to have a limited exposure for now, ready to increase in case of good news.

Oil: The party is not over

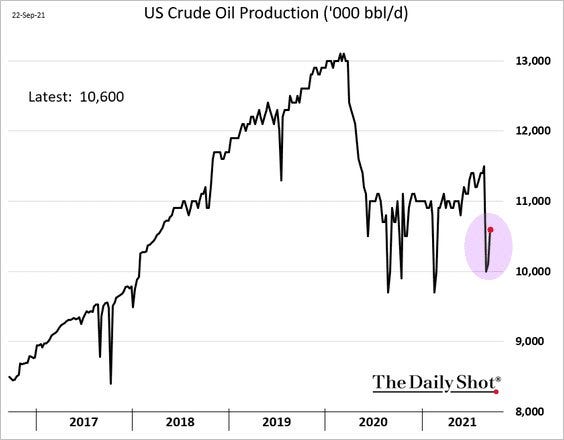

Last week I wrote that oil companies are worth a look, and I repeat it this week as well.

The impact of hurricane Ida has been high on U.S. oil production, that decreased sharply, and it could take weeks to go back at pre-hurricane level.

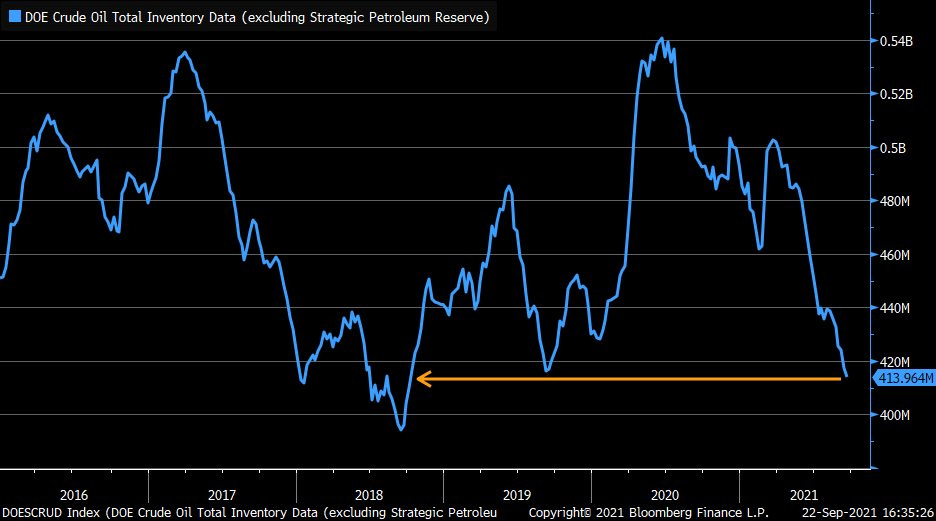

Moreover, the U.S. oil inventories are at lowest level of the last 3 years. This could be an indication of a deficit of supply with a healthy demand.

The oil price is at the highest of the last 2 months, and recently Goldman Sachs said that a colder than expected winter could drive oil price at 90$/bbl. I am not sure we will see that, but meanwhile I think that the sector could be an interesting investment area for the next months.

There are even risks on the horizon: new restrictions due to delta variant, an huge increase in output from Opec+ and, of course, a deeper crisis in China. If any of these risks will materialize, the bull thesis could be compromised.

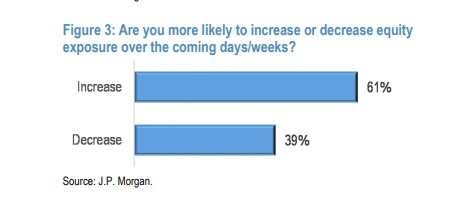

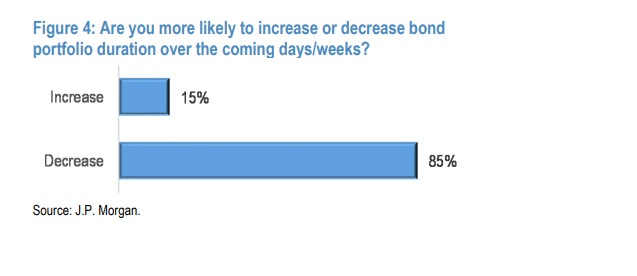

JP Morgan Clients Survey: Yes to Equities, No to Bond

The U.S. investment bank periodically asks to its clients how they are positioned and what is their current view of the markets.

More than 60% of clients said that they will probably increase their equity exposure over the coming weeks.

We cannot say the same for bonds: 85% of respondents think to decrease their bond portfolio duration. You want to decrease the duration when you see yields to go up (shorter bonds have lower impact on their price from the yield rise).

The last movement on Treasury yield could justify this fears…

Long live the stocks!

Have a nice weekend!

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.