Covid resurgence could derail the Santa rally?

Sensitive time for markets

Hello Guys,

Welcome back to “All Eyes on Markets”!

I hope you are all fine and I wish a happy Thanksgiving to all of you.

In case you haven’t subscribed to the newsletter yet, you can do it now. Just use the button below.

Let’s talk about markets!

4 more years of JPow

First of all I would like to mention that on Monday Biden decided to re-appoint Jerome Powell as Chair of Federal Reserve. This has not been a surprise, as the majority of investors already expected a second mandate for JPow. The unique other potential candidate was Lael Brainard, that has been nominated Vice Chair (and she is very dovish).

Despite the no-surprise event, markets reacted quite strongly to the news, and I would add that the reaction has been quite unexpected.

Just give a look to the 10-Year Treasury Yield, as of yesterday 25 November:

Powell is considered a dovish member of the Fed: in the last 4 years he proved to be very careful in taking any tight monetary policy decision. In the last press conference he was very reassuring as well.

Despite that, markets started to price a more aggressive approach from the central bank, and the 10-Year Treasury Yield started to increase significantly in few hours. Just think that investors almost fully priced 3 rate hikes before the end of 2022.

The Treasury Yield increase had a big effect on equities too: as already happened in the last months, higher yields impacted negatively on growth and tech stocks, and this time has been no different.

The impact on a “cyclical” index, like the Dow Jones, has been close to zero, while Nasdaq has been heavily hammered by rising yield and it lost 3.5% in a couple of market sessions.

This movement may have been a classic “sell on news”, but any furious yield rise can be worrisome.

I believe that markets assumed a too much aggressive approach from Fed, and previously they have been often disappointed by the Fed actual moves. Even this time I don’t see the central bank to make three rate hikes in 2022. There are several reasons behind my “conservative” assumption: firstly I still believe that once the supply chain bottlenecks will be eased, inflation will start to slow and it will take some pressure off from Fed members.

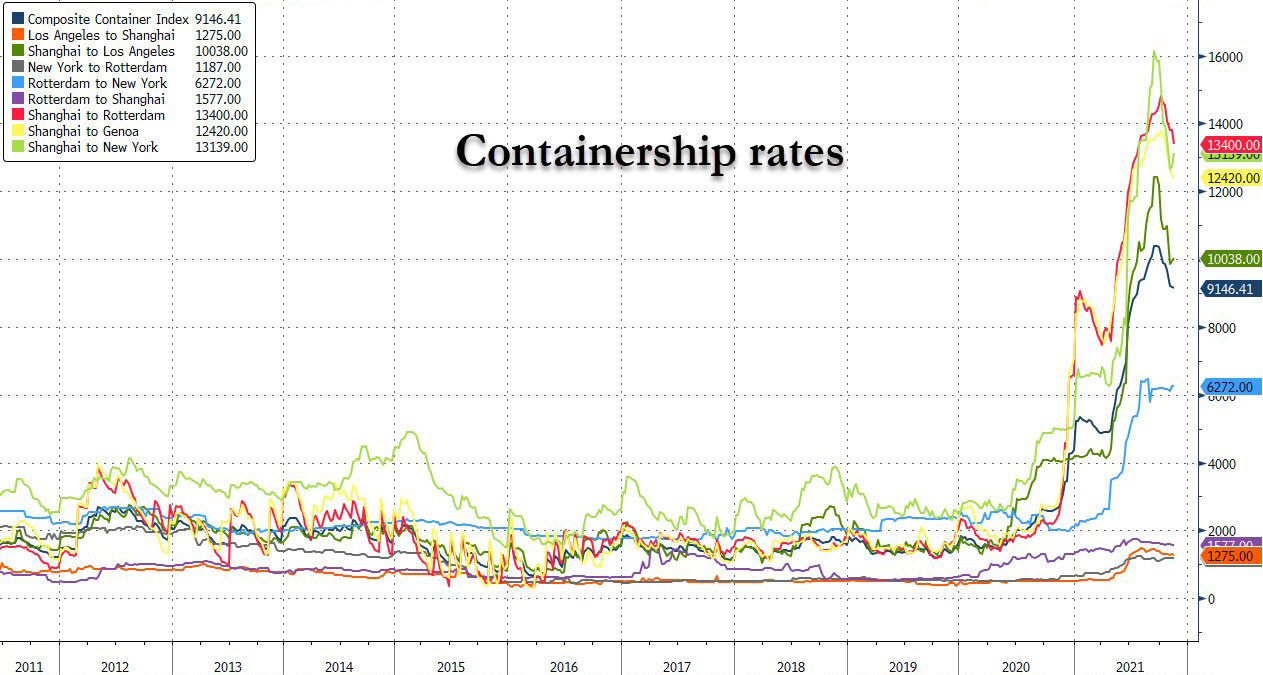

Containerships rates are already going down, and we will see soon if inflation will follow the same path.

Secondly, Covid resurgence in U.S. and Europe could create some concern on economic growth.

Covid update

In the last two weeks we read again several headlines on Covid cases rising and on new restricions.

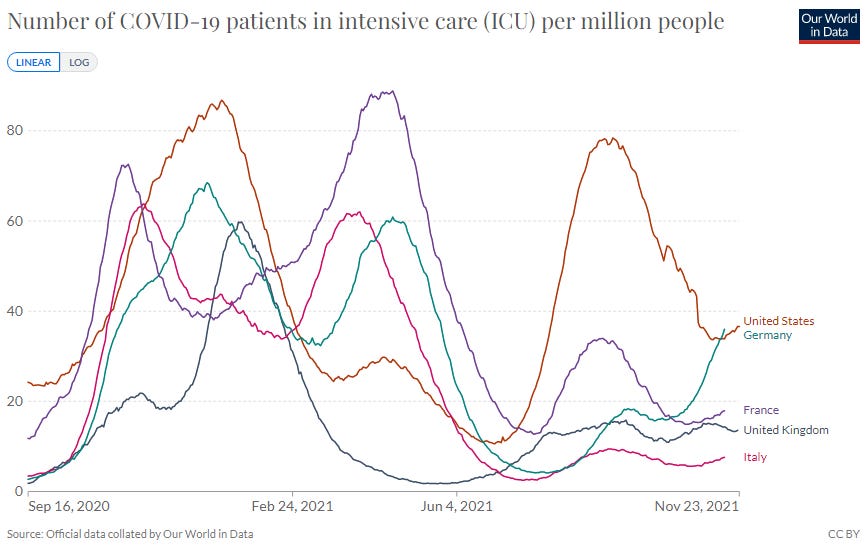

Let’s see the evolution of the pandemic:

As you can see in the charts above, currently there is an increase of new cases and of patients in ICU in European countries and U.S., especially in Germany (and in Austria and Netherlands too). So far, the most vaccinated countries as Italy, France, Spain and UK, are in a better situation.

It will be relevant to understand if governments will be forced to introduce new restrictions, as already happened in Austria. I think that governments will try to avoid as much as possible any restriction, but I wouldn’t rule out any potential lockdown in other part of Europe. Winter is coming.

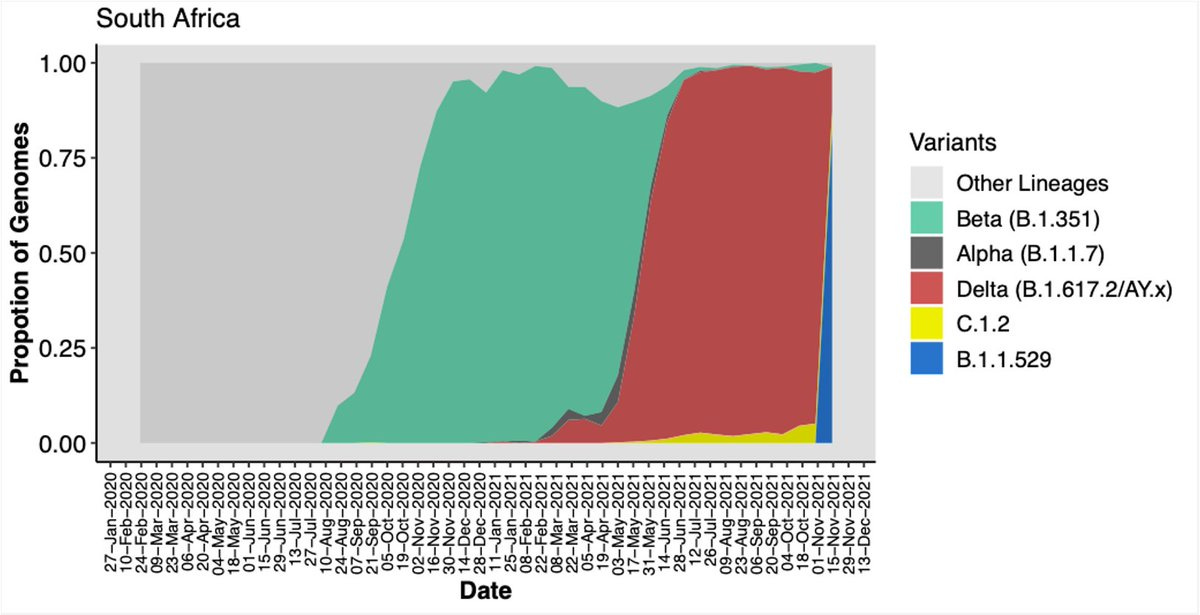

Moreover there is a new worrisome problem: a new Covid variant, called “B.1.1.529” and discovered in South Africa, where it quickly became dominant (see the chart below).

It will be very important to monitor any development related to “B.1.1.529” variant, especially if it can really substitute the “delta” one, and if vaccines are efficacy against “B.1.1.529”.

Where to invest now?

I think that currently there are not enough reasons to see rates to go up sharply: as said above, I think that inflation will cool down in the next months and the economic growth will be threatened by new possible restrictions. Central banks will not accelerate any restrictive monetary policy decision.

Today (Friday) markets are going down because of the new covid variant: as long as we will not have reassuring news about that, be ready for some market turmoil.

Fear of new restrictions (linked to higher cases and the new variant) will impact negatively on the following asset class:

Equities, especially on travel, value, and cyclical stocks

Oil

Emerging Markets

Generally on risky asset (crypto included)

On the other side there could be some defensive spot that will benefit from risk-off mode:

Government bonds (like Treasury, Bund)

Gold

lockdown winner stocks (Amazon, Netflix, Zoom Video, videogame, food delivery etc)

My suggestion is: don’t panic!

We don’t have any certainty regarding the new variant. Markets are in a panic selling mode.

Be ready for two hypothetical scenarios:

The new variant is bad and will force governments to introduce new restrictions. In this case it would be better to stay defensive!

The new variant is not scary: be ready to use your cash to buy the dip, and take advantage of lower prices for risky asset.

Follow my Instagram page if you want to be always updated on markets.

Have a great weekend!

Market Radar

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.