A frustrating month for markets

No signs of recovery for equities

Hello guys,

Welcome back to all of you, new and existing subscribers.

I really hope that you are good!

If you are reading this article but you have not subscribed yet, do it now! Use the button below!

If you want to have full access to two model portfolios (the Balanced Portfolio, Pure Stocks Portfolio), please consider to become a premium subscriber!

Let’s see what is happenings on markets.

After almost 2 years of rising stock prices, and falling yields, 2022 started in a frustrating way.

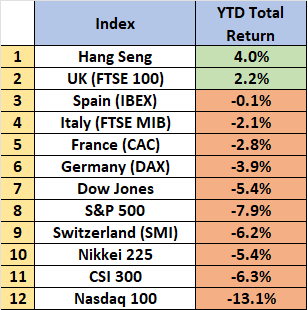

Most of the equity indices are negative YTD, and after the big fall in the first 3 weeks of the year, the reaction has been weak. Indeed many indices have been flat in the last weeks.

In any case there are still some bright spots as FTSE 100 (UK), Hang Seng (HK) and few other indices worldwide are positive:

Of course markets are now focused on 3 main themes: earnings, inflation and geopolitics.

With geopolitics I clearly refer to the Ukraine-Russia tension. Fears of a possible invasion in Ukraine are weighting on markets too, and investors are starting to put money on safe havens, like gold, Treasury and Bund.

Indeed gold just made a relevant breakout, and it is trying to go back to $2,000 per ounce.

I am not an expert in geopolitics and diplomacy, so I don’t know if Russia will really attack Ukraine (i hope not, but there is a chance to see that). In any case this tension can go on for a while, and it can lead to more volatility. Don’t underestimate that!

Q4 Earnings: good enough?

In the last few week investors have been focused even on corporate earnings: most of the S&P 500 companies reported their results for the fourth quarter of 2021.

How things are going?

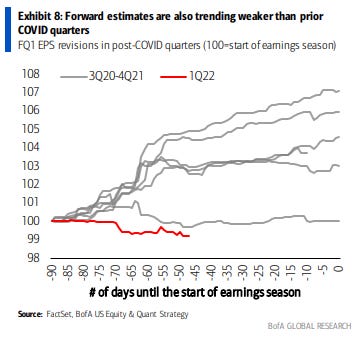

On average companies are going better than estimates, both on sales and earnings, but the average beat rate on earnings is the lowest since the beginning of the pandemic, and this is not encouraging.

Moreover forward estimates (for the next quarter) have been quite disappointing (worst quarter post-covid), as you can see below:

Finally, markets have been very severe with companies that missed earnings, and the average loss on earnings misses has been much higher than in the past (just think on how many companies have been hammered, like FB, PYPL, SHOP):

The above chart is useful to let you understand how stretched valuations were at the beginning of the year in few sectors (especially on growth stocks).

I would judge this earning season as good, but not great.

Fed: what are you going to do?

Another central theme is, of course, central banks!

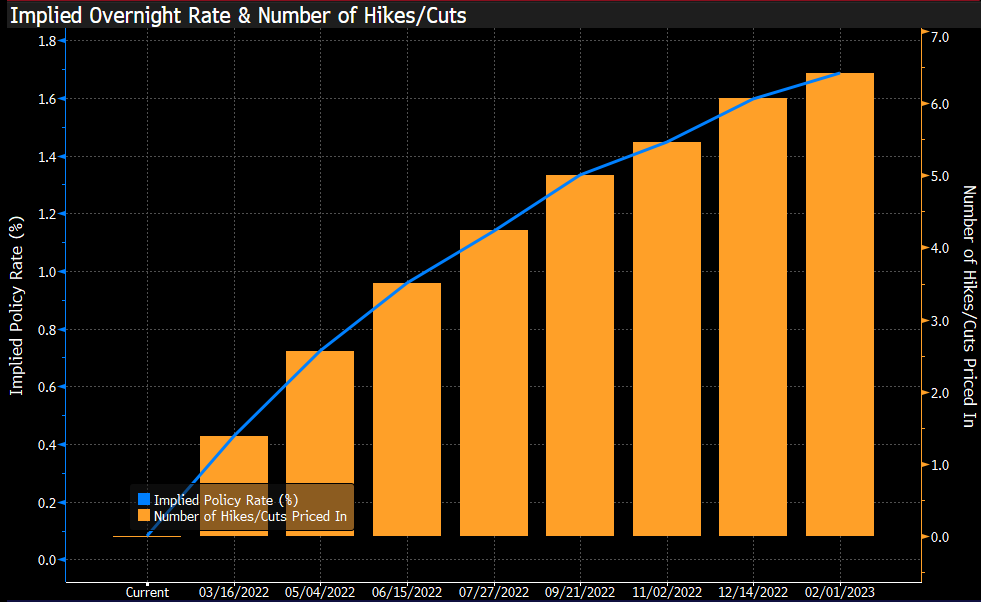

At the end of January some of the principal CBs (Fed, ECB and BOE) used very hawkish tones. The result? A generalized rise of yields.

Investors started to price an increasing amount of rate hikes (especially after CPI data above expectations). For example, now the implied number of Fed hikes for the year is 6.

For the ECB the implied number of rate hikes for 2022 is 2 (at the beginning of the year it was zero).

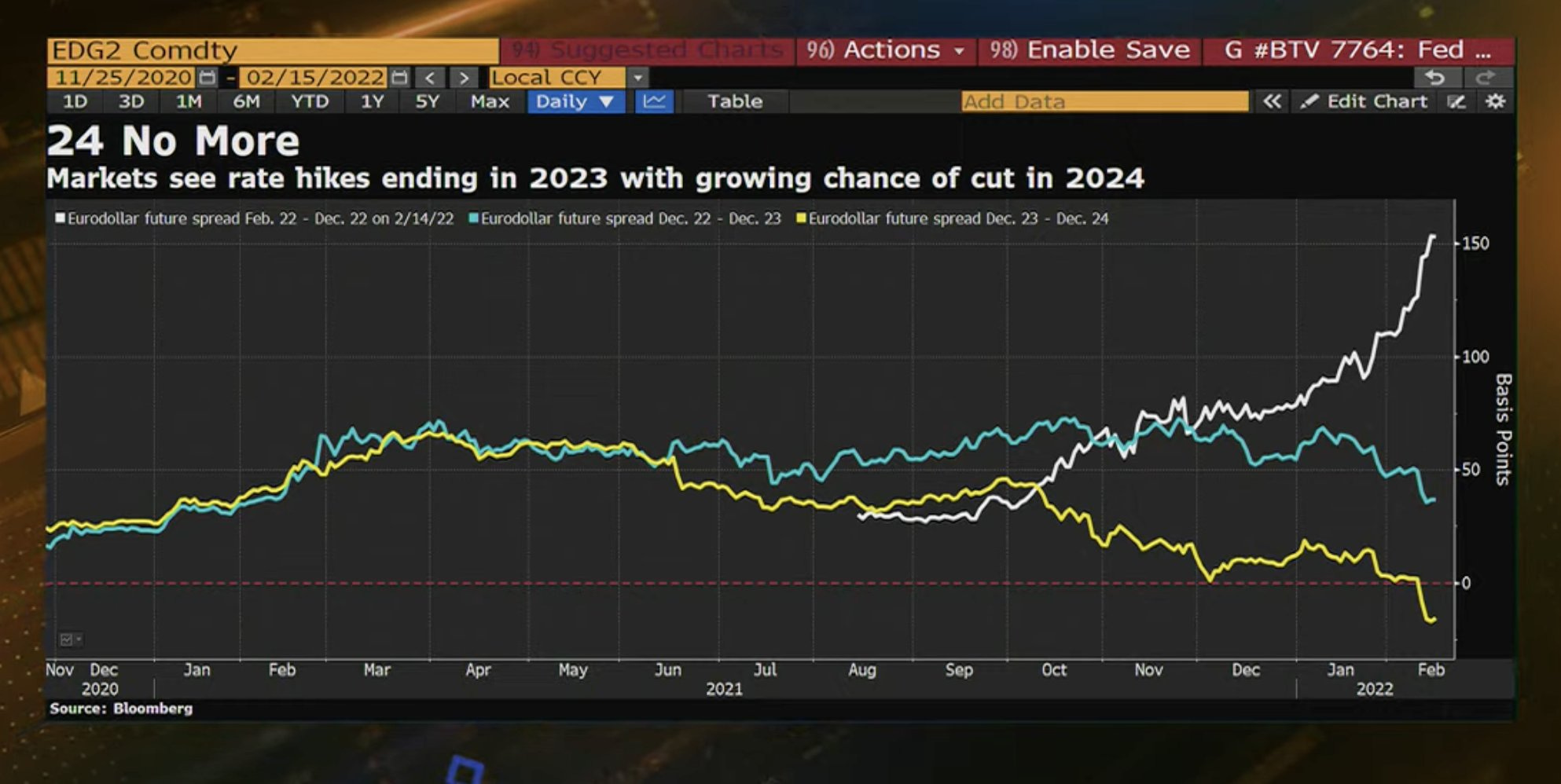

Furthermore it has to be said that markets are started even to price a new rate cut from the Fed in 2024.

So basically it is priced that the Fed will increase rates, but then it will be forced to go back: maybe markets are assuming that it is a mistake to be so aggresive in rising rates? Who knows…

Where to invest now?

Honestly I give a low chance to see six/seven rate hikes this year, for a couple of reason:

central banks do not have a clear plan, as even emerged from the last Fed minutes. So now investors are pricing future scenarios mostly based on their assumptions and not on Fed indications, and historically markets have a poor track record to forecast Fed moves.

Inflation could be close to the peak (just look at PPI in China), and if there will be a miss in the next weeks on any CPI or job data, there will be even less pressure on central bank officials.

For the above reason I think that the yield rise could be temporary done, and I am starting to look positively at bonds again. After the recent sell-off now yields are more attractive, especially in U.S.

In the last month the U.S. yields rose especially in the range 2Yr-5Yr, as you can see below.

I see interesting opportunities in short duration, both on government and corporate bonds. It can be a good idea to give a look and analyze some of the following ETFs: VGSH, VGIT, VCSH, SJNK.

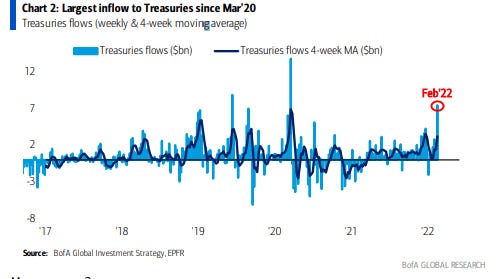

Moreover government bonds can be a good protection for the portfolio against any other geopolitical tension. Just look at the last week inflows to Treasury:

On the other side, equity is experiencing turbulent times, and I see volatility to remain here for a while (at least until we’ll see a real improvement in the Ukraine-Russia case).

Said that, the long term picture is still good, and valuations are now much more reasonable than they were few months ago.

The value rotation can still continue for a while, but I think that it might be wise to consider increasing the weight of tech stocks in the portfolio.

There are tech stocks that are down by more than 20% YTD, and now have low multiples. Here the list of the worst performers of Nasdaq 100:

Maybe you can find some opportunities in the list above.

In any case I strongly suggest to stay diversified: don’t go all-in on tech, but hold some cyclicals, like energy, financials, materials and industrials to balance the equity exposure.

Two weeks ago energy was my favorite sector (link here), but now I am slightly less positive on that: even if the demand is back at pre-pandemic level and production is still lower, I think that the upside for oil from the current price is more limited.

Moreover, as midterm election are coming, Biden will have to do all he can to ease pressure on oil prices: he already started to talk with Iran to find a deal on nuclear, and that could lead to the re-entry of 1.3 mln barrels/day in the market, a notable increase of the production. More actions will be probably taken.

Of course there are concrete chances to see oil price above $100, but I am now less confident on the sector.

I see more opportunities on financials and on travel & leisure. Both sectors are suffering these days from geopolitical tensions. If some kind of deal will be find with Russia, stocks related to those two sectors could really fly.

Finally, a mention on China: last year Chinese tech stocks have been hammered as CCP decided to act on internet-companies regulation, by imposing stricter rules.

Is the worst over? Tough to say, but in the last months the actions taken by the regulator have been less frequent (even if today Meituan plunged after the government issued new guidelines on food-delivery sector). Many chinese tech companies have ridicolous valuations, and it could be wise to look at them to diversify the portfolio and be exposed to different risk factors.

Even if 2022 has been frustrating so far, don’t desperate, better time will come!

Have a great weekend!

Market Radar

If you are a long-term investor, Please consider to become a premium subscriber. For a small price, you will have full access to two model portfolios:

Balanced portfolio (here the introduction)

Pure Stock Portfolio (here the introduction)

Moreover you will support my job here and on Instagram!

Disclaimer: Market Radar is not an investment advisor. Any information provided as part of the services is impersonal and not specific to any person’s investment needs. You acknowledge and agree that no content published or otherwise provided as part of any service constitutes a personalized recommendation or advice regarding the suitability of, or advisability of investing in, purchasing or selling any particular investment, security, portfolio, commodity, transaction or investment strategy.

Nice post.